|

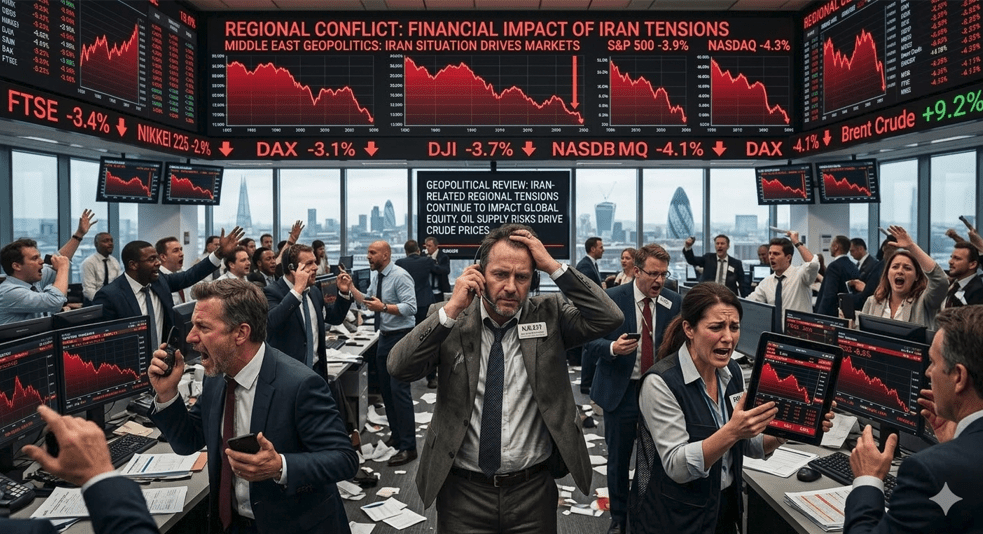

Before the launch of “Operation Epic Fury” the major U.S. stock market index was already trending in a sideways pattern since the October high. The growth sector was trending in a downward sloping way. With a surprise report indicating a weak jobs market and fears of further private credit losses, the disruption of oil supply from the Middle East is rising concerns of a U.S. recession – or worse – “stagflation”. So, the stock market again faces an Iran War with pre-existing conditions. Recent stock market action during conflicts underscored market resiliency. On June 13, 2025, when Israel began a bombing campaign against Iran’s nuclear and military sites, the S&P 500 fell 1.1% to 5,976 and dipped as low as 5,943. By the time the 12-day conflict ended, the index was up nearly 2%. On June 23, after the U.S. bombed Iran’s nuclear plants, the S&P 500 reversed higher and closed with a 1% increase. After that, the S&P 500index added nearly 15% before it took a 6% tumble in November. This January, the U.S. capture of Venezuelan leader Nicolas Maduro brought muted investor reaction. The S&P 500 rose 0.6% and the Nasdaq added 0.7% on the Monday that followed the weekend operation. The event didn’t alter the stock market’s dull trend. “Operation Absolute Resolve” was a short-lived military campaign, although it left questions about Venezuela’s oil industry and U.S. foreign policy.

As I noted above, the oil market is having the biggest impact on stock markets due to the Iran War. Whenever there’s a major military conflict in the Middle East, a close inverse correlation emerges between rising oil prices and falling S&P 500 returns. The 1990-91 Gulf War showed just that. We learned that oil price peaks can signal the lows for stocks, not necessarily military activity. Back then, oil prices topped and U.S. large-cap tech stocks troughed months before military action to liberate Kuwait even started because investors grew more certain that a combination of policy responses would resolve the conflict. So, oil price stabilization will be one of the primary signals for assessing current risk and a potential bottom. Since the start of “Operation Epic Fury” oil has been far from stable. Extreme volatility in oil prices has sparked a jump in the VIX (the investor “Fear Index”). Futures jumped sharply higher last Thursday on news that traffic had ground to a halt through the Strait of Hormuz. On Monday, crude futures soared above $120 a barrel but cooled off to $95 in afternoon trading as officials said they could tap reserves. Tuesday delivered fake news that the U.S. Navy had successfully escorted an oil tanker through the Strait of Hormuz. Instantly oil crashed 17%. After that report was denied, oil shot up from about $78 to near $90, a 15% pop. Market sensitivity to news about the Strait of Hormuz makes sense. The Strait is the primary conduit through which oil and liquefied natural gas exports pass from Saudi Arabia, Iraq, the United Arab Emirates and Kuwait, as well as Iran. Some 80% of Saudi exports reportedly exit the Persian Gulf into the Gulf of Oman. Saudi Arabia is moving some Persian Gulf exports to the Red Sea via a pipeline, but not without risk and well short of usual export flow.

The Iran war has rattled foreign stocks more than U.S. equities. For many foreign indexes, the damage so far has rivaled that of last April when Trump’s tariffs sent shock waves across global markets. U.S. stock market indices are mostly in a trading range. One of the smartest stock market operators alive is Mark Minervini, author of “Trade Like a Stock Market Wizard”. He says, “History shows that conflict-driven declines eventually create meaningful buying opportunities — but not immediately. Risk is elevated, and patience is required. This too will resolve. And when it does, a new up-leg will emerge from the geopolitical rubble — as it always has.”

|