|

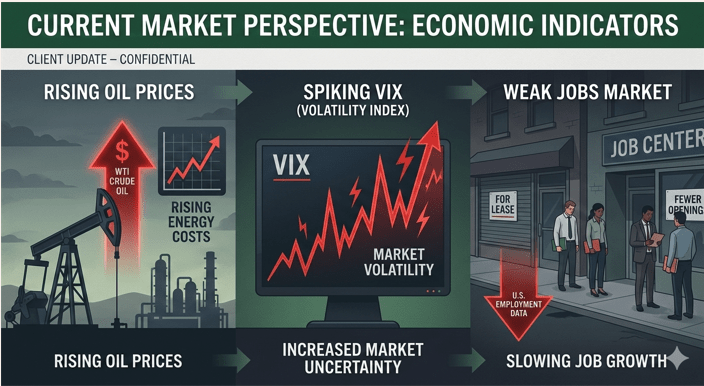

Perspective is essential for investors. This week’s financial market action is a reminder of that truth. From a macro market perspective, this week could be summed up with “Up, up and down.” Oil and volatility (measured by the VIX – “fear index”) were up. Jobs were down.

Since the U.S. and Israel have launched strikes against Iran last weekend oil has gone up. Saying oil is up this week is an understatement. WTI Crude has spiked over 36% since last Friday. Today’s close above $91 was the highest since September of 2023 and was the biggest weekly gain in futures trading history in 1983. Oil prices jumped over 12% today alone on fears triggered by news commentary that it could rise to $150 a barrel in coming weeks. The key consideration impacting oil prices so far is the Strait of Hormuz, a crucial waterway that connects the Persian Gulf to the rest of the world. Oil markets have been volatile on news of attacks on oil tankers on the one hand, and commitment by the U.S. to provide safe passage and insurance on the other. Basic supply and demand dynamics are clearly a force. This has been exacerbated by reports that countries like Kuwait may be cutting production.

The other “up” is the VIX (known as the fear index), measuring expected market volatility. The volatility index soared over 24% today. It closed under 20 last Friday and closed near 30 today. The near 50% spike in the VIX is a manifestation of investor FUD (fear, uncertainty and doubt) caused by the Iran conflict and concerns over how higher oil prices could impact the economy.

Now, the down. Jobs. Today’s jobs report was unexpected. Economics polled by The Wall Street Journal had forecast 50,000 new jobs last month. The Bureau of Labor report showed total nonfarm payrolls fell by 92,000 in February 2026, the worst reading since last October, with average monthly job gains over the past year coming in at just about 19,000. Payroll numbers for the past two months were also revised down by 69,000 jobs, a significant amount. This is continued evidence that the labor market has slowed considerably. Making the jobs picture look worse, the unemployment rate rose only slightly to 4.4% from 4.3%.

What we have in the markets now, more than usual, is a lot of “noise”. Speculation today of oil soaring to $150 sometime soon was the loudest. Investor’s perspective on the up’s and down’s of the week should keep the current situation context relative to their investment plan and realistic economic impacts. This week’s combination of soaring energy costs and a cooling labor market has created a classic “stagflationary cocktail” that is testing the market’s resilience. Economists expect a $10 rise in oil per barrel to cause gas prices to increase by 25 cents per gallon. A sustained $10 increase in oil prices is estimated to cause a 0.1-.03 percent drop in U.S. GDP. Add that perspective to a weak jobs market. Today’s weak jobs report for February quashed the notion that the labor market is stabilizing, but it likely won’t push the Federal Reserve to cut interest rates this month, given the oil price shock from the Iran war poses a risk of higher inflation. The situation that has evolved this week puts the Fed between a rock and a hard place. A continued weakening in the labor market would support a rate cut, but given the risk that higher-for-longer oil prices could trigger another inflation surge. The Fed could choose to stay in sidelines. This would require a market adjustment as interest cuts have been expected this year. Finally, the S&P 500 closed over 7,000 for the first time at the end of January. After all the ups and downs of this week highlighted by a sharp spike in investor “fear”, the major market index closed at 6,740 – just about 3% off its all time high.

By framing market volatility as a normal part of the investment cycle, investors can maintain better, more rational, and patient decision-making.

|