|

Since the first strike of Operation Epic Fury on February 28, there hasn’t been a single news cycle where oil didn’t command front-page real estate. The war with Iran has caused a global “energy shock”. Because the conflict isn’t just a regional border dispute—it’s a direct chokehold on 20% of the world’s petroleum and LNG—the price of crude has become the “scoreboard” for the war. Even on days when the military headlines were massive, oil remained the primary sub-headline or the “lead economic” story. In the eyes of the editors, the “Oil Story” is the only one that hits every single reader’s wallet, making it the most reliable headline since the war began.

First thing I read yesterday was a news article, “We are seeing a stronger open on Wall Street this morning, as oil prices are sliding on hopes of a truce between the U.S. and Iran. U.S. benchmark WTI crude is back below $90 a barrel.” When I picked the Wall Street Journal I saw the lead article, “Oil Supply Crunch is Spreading From Mideast to Rest of World.” The previous day it was, “Iran’s Strikes Are Costing Big Oil.” In evening news earlier this week “Peace Hopes” dominated the news with headlines such as “Markets Rally as Energy Supply Fears Recede.” I was surprised to not see “OIL” make the Journal’s front page headlines today, but there it was in the section on World News as the lead article, “A Global Energy Safety Net is Unraveling”. And so on, and so on…. On Wall Street it’s now all about oil. Here’s some perspective on the oil shock:

The economics of the war are expected to be high and long-lasting – having a direct effect on oil. Damage to oil-and-gas infrastructure in the Middle East caused by the war with Iran will take years and billions of dollars to repair, which would hamper efforts to fully restore production even if the conflict were to end soon. One analyst put a price tag on estimates to fix it at least $25 billion, and possibly more. It is expected that even after the Iran War ends, it will take months for Iran and its Middle East neighbors to return to their full pre-war oil production levels. Energy intelligence company Enverus forecasts international oil prices to average $95 in 2026 and $100 in 2027. Analysts estimate that more than six million barrels of oil production a day, and perhaps more, has already been shut in by Gulf countries.

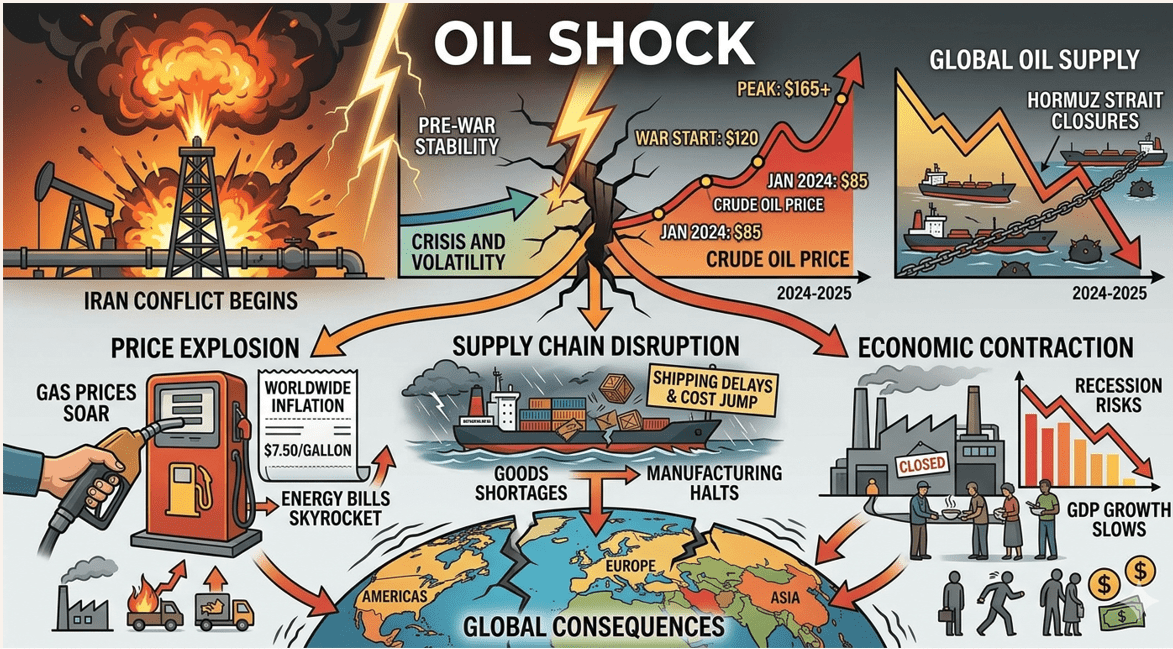

The Strait of Hormuz is essentially closed as traffic is now down about 95% from pre-war levels. The effective closure of the Strait of Hormuz on March 4 has stranded approximately 20 million barrels per day (mb/d) of oil and petroleum products, representing roughly 20% of global consumption. Major Gulf producers (Saudi Arabia, UAE, Kuwait, and Iraq) have collectively cut production by an estimated 10 million barrels per day (mb/d) as of mid-March. This is largely due to the exhaustion of local storage capacity and the lack of viable alternative export routes. Fuel prices continue to be big concern as supply constraints persist. Chevron’s president of downstream said he is concerned about California’s fuel supply, suggesting that after a jump in prices, the next impact could be lack of available gas. Chevron CEO Mike Wirth states energy markets are underpricing the oil supply shock from the Iran war, with futures not reflecting physical impacts.

The macro supply/demand picture has been shocked. Prior to the conflict, Iran was producing roughly 3.5 mb/d of crude and exporting about 1.7 mb/d. In January 2026, the global market was comfortably supplied, with production at 106 mb/d slightly outpacing a demand of 104 mb/d. This “supply glut” initially tempered the war premium, but the total blockade of the Strait has since flipped the market into a structural deficit of 5–8 mb/d.

Oil prices climbing higher are a direct inflationary force. Costs rise in critical economic sectors from transportation to manufacturing and goods. Worst case is sustained high oil prices fuel “stagflationary” pressures, reducing consumer spending and potentially inducing recessions. Economists estimate that every $10 per barrel increase in oil adds 0.2% to inflation. Before the initiation of strikes on February 28, Brent crude was trading at approximately $66 per barrel. Since the onset of hostilities and the subsequent closure of the Strait of Hormuz, prices spiked to a peak near $120 before settling into a volatile range between about $90 and $115. So far in the U.S., gasoline prices have surged between 5 and 10 cents daily in some regions, with national averages rising from pre-war levels to over $4.00 per gallon — the highest since late 2023.

Restoring supply to keep prices stable may be difficult and will likely take time. It could take months to declare the waters fully safe for commercial tankers to move oil through the Strait. LNG facilities are particularly difficult to “cold start.” Even upon a diplomatic resolution, experts suggest it would take several weeks to reach pre-war delivery levels. In an emergency move, and the largest coordinated action in its 52-year history, the International Energy Agency (IEA) has authorized the release of over 400 million barrels from strategic reserves to bridge the gap, but at a maximum draw rate of roughly 4–6 mb/d, this only partially offsets the daily shortfall. The latest data on alternative bypass infrastructure confirms that while these routes are being pushed to their absolute mechanical limits, they can only replace a fraction of the 20 million barrels per day (mb/d) typically transiting the Strait of Hormuz. It is expected that even if every bypass pipeline in the Middle East operated at 100% efficiency, they could only handle about 45-50% of the volume lost from the Hormuz closure. This leaves a “homeless” volume of roughly 10–13 million barrels per day that simply cannot reach the market, regardless of production levels.

The consensus among major forecasting bodies as of yesterday is that the current oil price spike is a temporary, war-driven supply shock that will be followed by a gradual return to a lower-price environment (likely in the $60-$70 range) as markets adjust and supply increases elsewhere. If not, inflation concerns will become a larger threat and will likely spark more talk of “stagflation”. Such a high inflation + low economic growth condition would call for a defensive investment strategy.

Keep reading headlines. The oil story will be told for a while.

|