|

Recapping Last Week

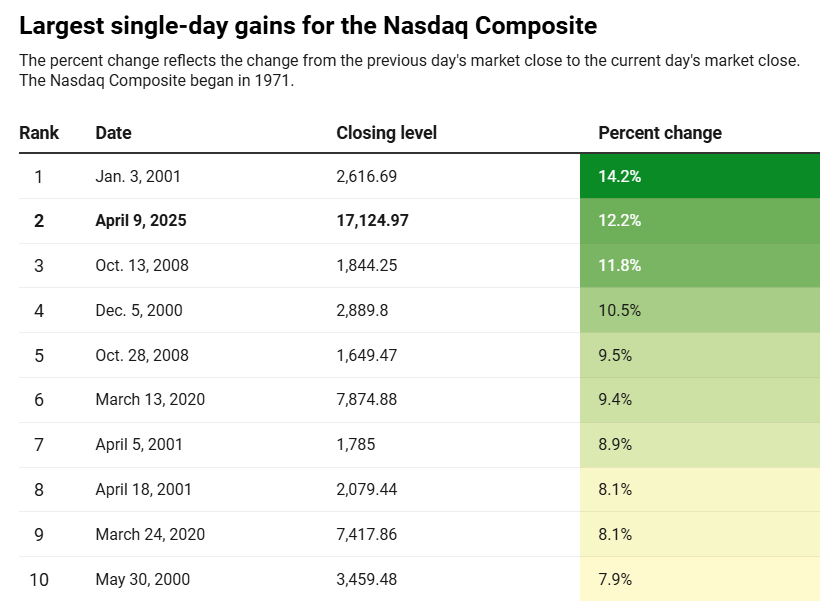

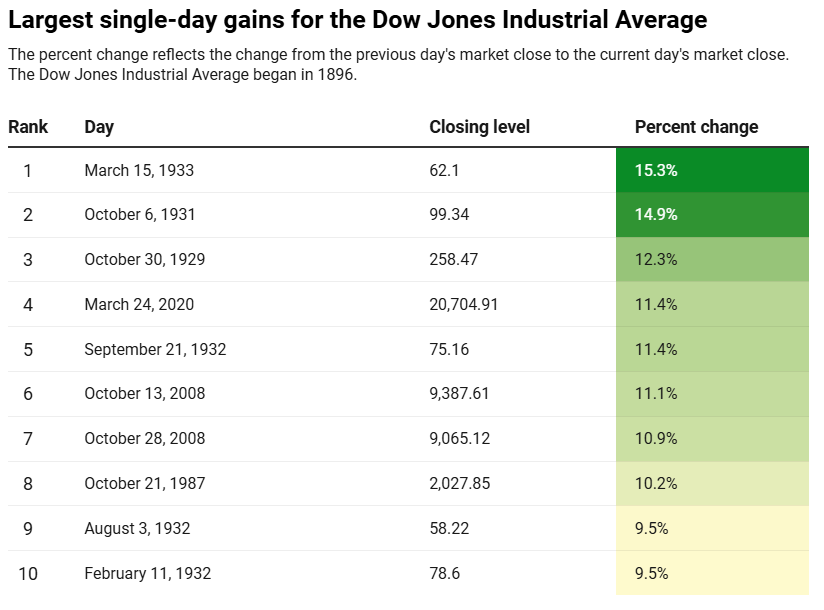

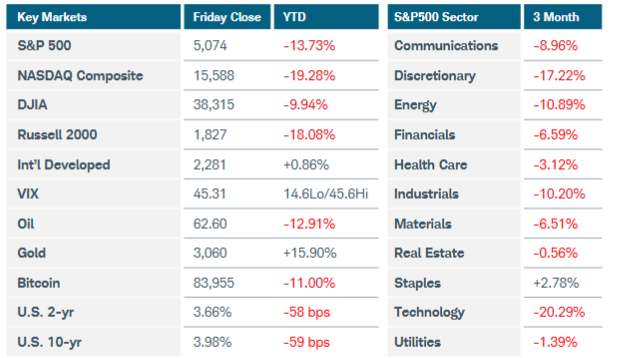

Risk assets plunged around the globe as larger than expected tariffs imposed by the U.S. along with retaliations by major trading partners such as China stoked recession fears. After a modest rally to begin the week, the S&P500 index tumbled nearly 5% on Thursday and another 6% on Friday, finishing 9% lower overall. The Nasdaq Composite sank 10% as technology stocks were hammered, while the Russell 2000 also lost 10%. The Cboe volatility index soared above 45—a level not seen since August—implying an expected daily move greater then 2.8% for the S&P500 index. Crude oil prices plummeted more than 9%, dragged down by fears of a global trade war along with OPEC’s surprising decision to increase oil output by a higher-than-expected 411,000 barrels per day starting next month. Investors flocked to the safe-haven of fixed income investments, sending the 10-year U.S. Treasury yield below 4% for the first time since October. The U.S. dollar fell sharply against other global currencies, reflecting concerns that a trade war could impact domestic growth more than other economies. In a speech Friday, Fed Chair Powell said he expects tariffs to raise inflation and slow economic growth, but indicated the FOMC won’t move on interest rates until the impacts are clearer. Turning to other economic news, U.S. job growth was stronger than expected in March, providing at least a temporary reprieve from the flood of negative data. Nonfarm payrolls increased by 228,000 with the unemployment rate ticking up only slightly to 4.2%. Layoffs surged last month and in the first quarter according to the Challenger report but have not shown up in the official labor market data as court cases contesting the firings are pending. The ISM manufacturing PMI slipped into contraction for the first time this year, registering a 49.0 reading in March. The prices paid index jumped to the highest level in nearly three years, and survey participants indicated much uncertainty. Growth in the services sector stalled as the ISM’s measure of employment contracted for the first time in six months.

In international markets, Europe and other developed markets gave up most of their gains for the year. The MSCI EAFE index sank more than 7% as the realities of a potential trade war set in. Inflation in the Eurozone edged lower in March, lifting expectations for another rate cut at the next central bank meeting later this month. The Reserve Bank of Australia opted to keep interest rates unchanged and wait for upcoming inflation and labor market data before committing to future rate cuts. Finally, China’s manufacturing and services sector activity showed promise last month, according to the official government and Caixin PMI surveys. Rising trends in new orders and employment may have represented temporary lifts ahead of last week’s tariff news.

Current View

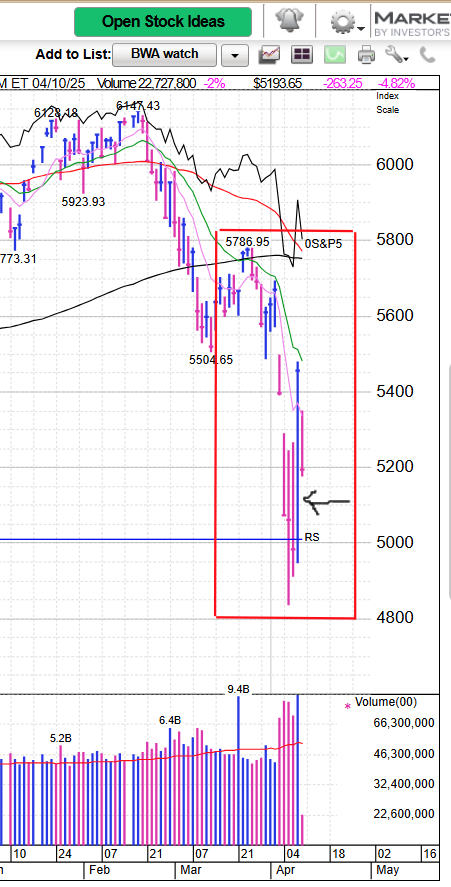

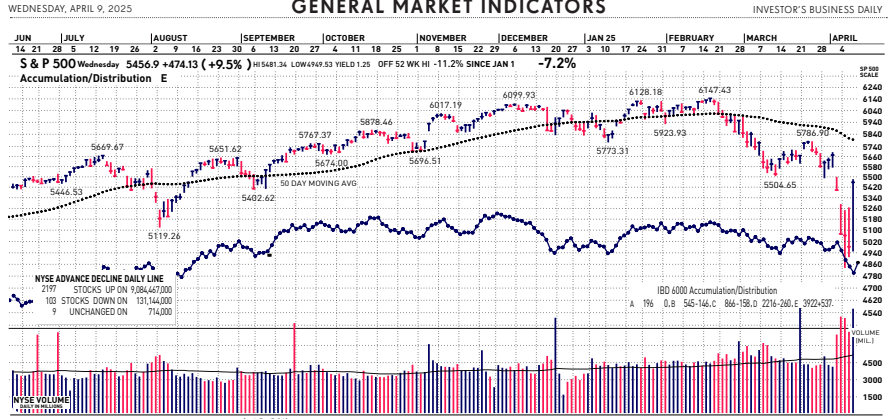

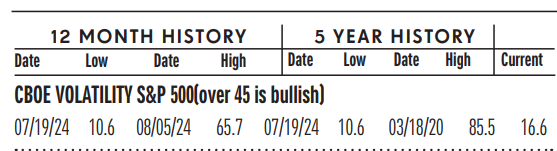

At the end of last week’s collapse in U.S. equity markets, some signs of capitulation emerged. Friday’s decline was among the worst breadth days in the last 60 years, registering a Major Distribution Day in terms of both declining issues and volume. From a technical perspective, the Nasdaq-100 index experienced a drop of more than 20% from the February 19 high to Friday’s low. Those were reliable indications that the general stock market was due for a bounce. Tariff talks are on-going, including as I write today’s ERPE Excerpts. So, extreme volatility and investor uncertainty remain. Sellers came out in force and pounded stock indexes today after it was reported President Donald Trump said new tariff rates on Chinese goods would climb higher than expected. Even tame inflation news couldn’t stop selling so far today. Volume jumped 35% above average. Decliners are outpacing advancers 9-to-1. The macro market is near bear market levels.

|