|

The History of Tariffs and Their Impact on the U.S. Economy

Tariffs have been a critical component of U.S. trade policy since the nation’s founding. They serve as taxes on imported goods, aimed at protecting domestic industries, generating government revenue, and influencing economic behavior. Understanding the historical context and effects of tariffs can provide valuable insights for high-net-worth individuals regarding potential impacts on investments and the broader economy.

Early History and Purpose of Tariffs

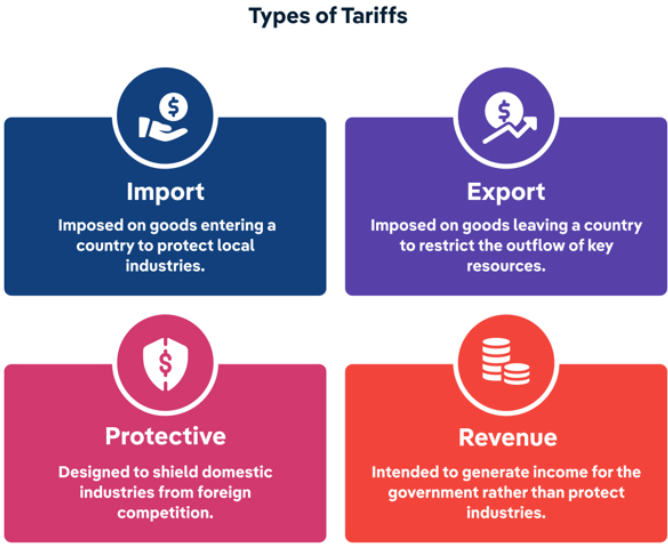

The U.S. Constitution grants Congress the power to impose tariffs, a tool which was initially used to fund the federal government and protect emerging industries. The Tariff of 1789 marked the first major legislative use of tariffs, primarily intended to generate revenue. Over the 19th century, tariffs evolved into protective measures that helped developing American industries compete against established foreign competitors.

The Role of Tariffs in Economic Policy

Throughout history, tariffs have fluctuated in response to global economic conditions and domestic priorities. Major tariff acts, such as the Tariff of 1828 (the “Tariff of Abominations”) and the Smoot-Hawley Tariff of 1930, showed the potential for tariffs to spark trade wars and economic downturns. The latter is often credited with intensifying the Great Depression by stifling international trade. Tariffs saw a decline mid-20th century as the U.S. shifted towards free trade to stimulate economic growth. The General Agreement on Tariffs and Trade (GATT), established in 1947, aimed to reduce tariffs and promote international trade, leading to significant economic expansion.

Recent Trends and Modern Implications

In recent years, especially starting in 2018, tariffs have resurfaced as a significant part of U.S. trade policy, notably during the trade tensions between the U.S. and China (and Mexico, Canada and Europe). The imposition of tariffs on goods from China was aimed at addressing trade imbalances and protecting intellectual property rights, but it has also led to retaliatory tariffs, which disrupted global supply chains.

For investors, the implications of tariffs can be sizeable. Tariffs can elevate costs for companies reliant on imported materials, affecting their profitability and stock prices. Additionally, consumers may face higher prices on goods subjected to tariffs, potentially leading to reduced spending and slower economic growth. These, for example, are the very issues GM is leaning into as I write this.

Strategic Considerations for High-Net-Worth Individuals

Understanding the potential impact of tariffs on investments and the economy is crucial for investment strategies. Investors should consider:

- Sector Exposure: Industries such as manufacturing, agriculture, and technology may respond differently to tariff changes. Diversification across sectors can mitigate risks. There has been Trump tariff talks on a wide of products since the Campaign Trail – ranging from steel and cars, to Champagne and pharmaceuticals.

- Global Supply Chains: Some companies that have adaptive supply chain strategies, enabling them to navigate tariff impacts effectively.

- Economic Indicators: Stay informed. Keep perspective and a long term view. Monitoring macroeconomic indicators such as inflation, consumer spending, and trade balances can signal broader economic conditions.

The history of tariffs in the U.S. reveals their complex role in shaping economic policies and impacting markets. The Smoot-Hawley Tariffs is considered one of the most catastrophic congressional Acts in history, though it was well intended. By understanding historical precedents and current trends, investors can be better positioned for both challenges and opportunities that tariffs present. So, with “Liberation Day” on April 2, we will gain more insight on the scope of the developing trade war. Let’s hope it is not a repeat of the 1930 “Mother of all trade wars”.

|