|

Recapping Last Week

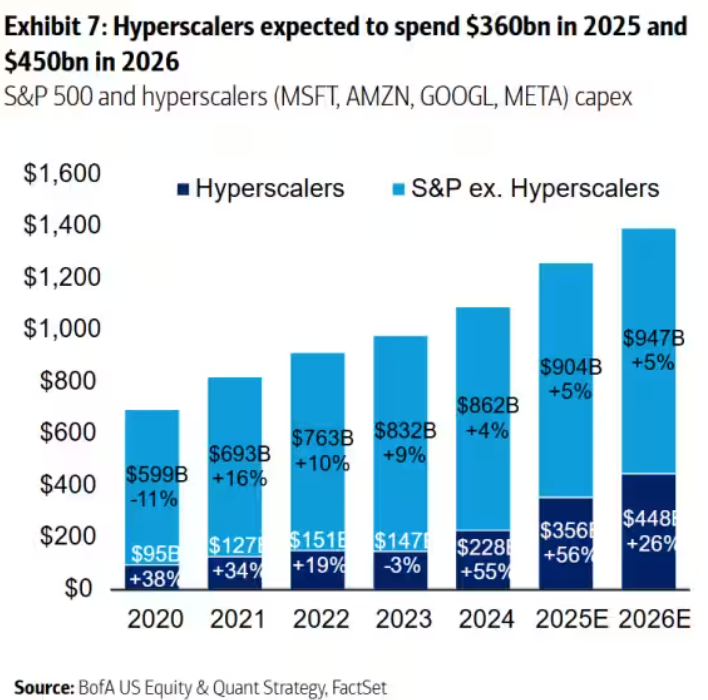

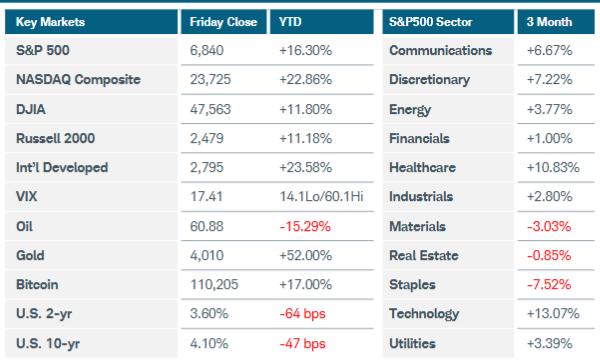

Strong earnings reports from some of the “Magnificent 7” technology companies boosted the Nasdaq Composite index by 2.3%, while U.S. Treasury yields rose after the Federal Reserve lowered interest rates but made statements leading to uncertainty about further cuts this year . The S&P500 gained less than 1% while Russell 2000 slid 1.3%, pressured by a rising U.S. dollar. Sector performance tilted negative despite technology’s strong showing. Sectors representing real assets slumped after trade talks between the U.S. and China resulted in a de-escalation of tensions over issues like rare earth exports, although root causes of the conflict remained unresolved. Crude oil prices fell 1% after news emerged that OPEC+ is leaning towards another modest output increase for December. Gold futures fell for a second straight week but stayed above $4,000 per ounce. Investors were wary of huge artificial intelligence investments by U.S. firms like Meta Platforms and Microsoft but were reassured by Alphabet’s ability to fund its plans from current cash flows and Amazon’s strong forecast. Turning to monetary policy, Fed Chair Powell acknowledged there were “strongly differing views” about how to proceed in December, given the lack of official government data. His comment that another rate cut is “not a foregone conclusion” was slightly unnerving to stock and bond investors, although by week’s end the effects were muted. Odds for a December rate cut fell to around 65%, based on fed funds futures. The Fed also announced it would restart limited purchases of Treasury securities to maintain ample liquidity in the banking system. Meanwhile, the U.S. government shutdown extended into a fourth week with no signs of a resolution, and economic data remained sparse. Research firm ADP announced it would release a weekly estimate of the change in private sector employment in addition to its regular monthly report. While the added transparency may help, it still represents a far-from-complete picture of the U.S. labor market. A Chicago Fed estimate showed the September unemployment rate likely stayed steady at 4.3%, although ADP noted that corporate layoffs increased notably last week. Consumer confidence fell in October on dimmer views for the economy and labor markets. Mortgage rates dropped for a fourth straight week, boosting refinancing activity and new applications.

Overseas, the Bank of Japan kept rates unchanged but delivered its strongest signal yet that a hike was possible soon. Inflation accelerated to 2.8% in October, well above the central bank’s 2% target. The European Central Bank also left rates unchanged and offered no clues about future moves. Economic growth has remained steady in the Eurozone despite trade turbulence while inflation hovered near the bank’s goal. The Bank of Canada cut rates by 25 basis points, citing a weakening economy as the impact of U.S. tariffs is becoming more evident. Finally, China’s manufacturing activity contracted more than expected last month while services stayed in expansion territory.

Current View

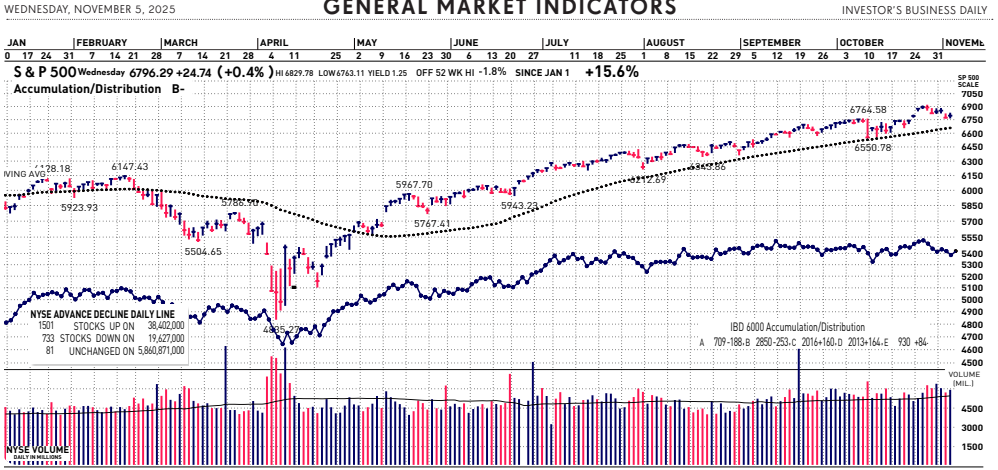

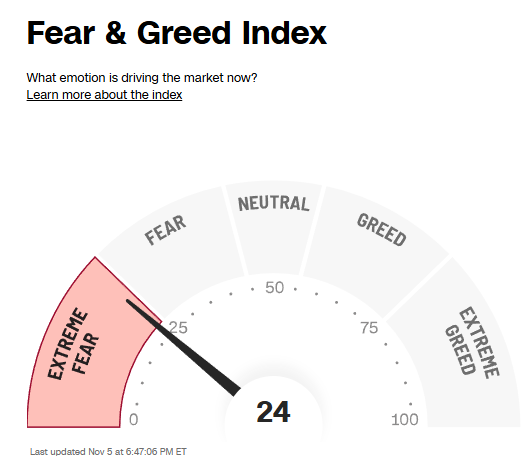

Major market index price swings are displaying yo-yo like action. The recent volatility has put the stock market’s directional trend in question. However, notable price declines such as the SP500 down 1% or more in a day has only happened 4 times this year since May 1. And today is one of them. For perspective, the annual average daily decline of 1% or more for the SP500 since 1958 is 23. Momentum appears be turning from highly valued tech stocks as earnings reports are pouring in daily. Some analysts are heard saying soaring stock gains have priced them for “perfection”.

For perspective, this year’s stock market gains going into November bode well for the last 2 months of the year. When the SP500 has been up 15% or more going entering November, it has climbed higher 20 out of the 21 occurrences through year end.

|