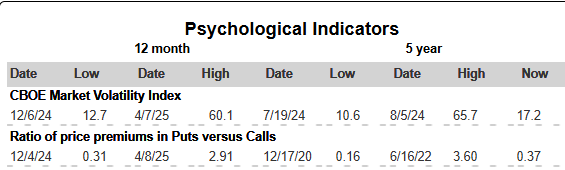

|

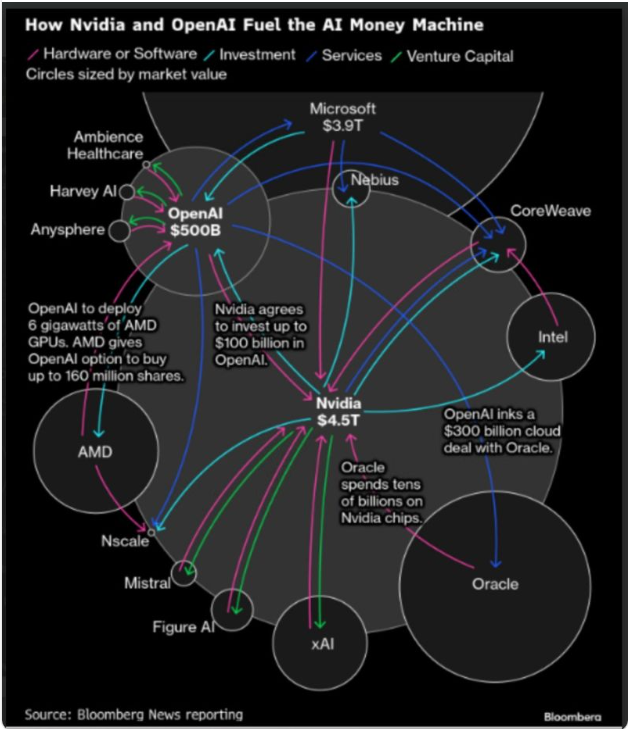

The term “circular spending” can refer to two very different concepts: a potentially misleading and problematic financing technique in the business world, or a macroeconomic model for how money flows through an economy. This term has been brought up a lot lately – with reference to its less-than-positive version. Recently, discussions of “circular spending” have caught my attention nearly daily is they relate to veritable frenzy of spending in AI. Investments over the last couple of years is measured in hundreds of billions of dollars in private and government funding, with corporate spending and committed capital for infrastructure driving the total expenditure well into the trillions over the near future. The last two years represent an inflection point where AI has become the dominant destination for tech investment globally. Global AI spending is projected to approach $1.5 trillion in 2025 and maybe $2 trillion by 2026. This includes enterprise spending on AI services, software, and infrastructure. Here is a simple idea of how “circular spending” works in a potentially unsustainable way between two companies: Company A invests money in Company B. Company B then uses that money to buy products or services from Company A. This “round trip” of cash makes it appear that both companies have healthy, growing businesses, but it is not based on real demand or outside customer spending. I thought of a kid setting up a business with a neighborhood lemonade stand. The kid gives his friend money to buy a cup of lemonade. The friend “buys” the lemonade and the entrepreneur kid calls that money received a “profit”. The graphic above shows the flow of big money between AI related companies. Note the round trip flows out of and into Nvidia. I call this “boomerang bucks”.

This business-to-business practice was a hallmark of the dot-com bubble of the late 1990’s and early 2000, where telecom companies and internet startups inflated revenue figures by buying services from one another. When the bubble burst, many of these companies collapsed. That memory has many old Wall Streeter’s, like me, a bit concerned. Of course, one can also hear today that, “It is different this time.” The fact is there have recently been major investments by tech companies in AI startups, with the startups in turn purchasing a large amount of hardware from their investors. Different? We won’t know how the surge in investment, enthusiasm and euphoria in the new technological revolution ends until it ends.

The “circular spending” in AI has is another reason for one of the most common questions today: “Are we in an AI bubble?” Here’s how some knowledgeable tech experts and experience money managers answer the question.

“Are we in an AI bubble? Of course! Of course we are. I mean, we’re hyped, we’re accelerating, we’re putting enormous leverage into the system,” said Pat Geisinger, former Intel CEO.

“We’re certainly seeing lots of evidence of bubble-like behavior in the AI space. We see the kind of circular revenue deals, we see a lot of very aggressive price behavior,” said Ben Inker, Co-Head of Asset Allocation at GMO.

And, finally, Howard Marks, Co-Founder of Oaktree Capital Management said, “To me, the main ingredient in bubbles is psychological excess — there’s no such thing as a price too high. And I don’t detect that level of mania at this time, so I have not put the bubble label on this incident.”

To me the balloon is holding a lot of air, but with more room before it pops. I experienced the day by day – really, hour by hour – mania leading up to the dot-com bubble implosion. This when I first lived what FOMO means. People actually had a fear of missing out. The Nasdaq index soared over 50% from late October of 1999 through year end. And then it jumped another 25% by March 1, 2000. That’s all after a phenominal bull market in the Nasdaq that went up 10x from April of 1991. The great 1990’s dot-com bull market bubble popped only after investors lost control of rational behavior – when it was thought that no price was too high. We are not there… yet.

|