|

Bi-MONTHLY MARKET ANALYSIS &

ECONOMIC UPDATES

|

|

|

May 7, 2026

Abel Era

The New Operator in Omaha

|

|

|

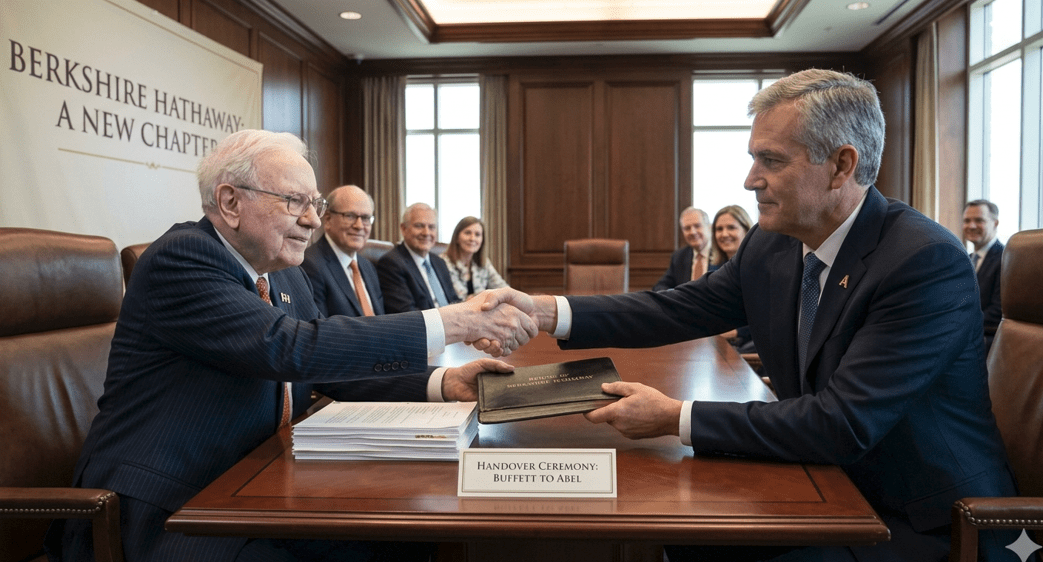

Call it “The Berkshire Baton”. There’s been a big hand-off at the trillion dollar company in Omaha. Mr. Warren Buffett has handed the reigns of Berkshire Hathaway to a new CEO, Mr. Greg Abel. This past weekend was the first Berkshire shareholder meeting hosted by the company and conducted by someone other than Warren Buffett in a long time. In addition to the fanfare and main attractions in Omaha each year at the shareholder meeting, investors worldwide have also looked forward and enjoyed reading the annual letter to shareholders from the company -specifically from Warren Buffett. For over half a century, the Berkshire Hathaway annual letter was more than a financial disclosure; it was a fireside chat with the “Oracle of Omaha.” We could read for the wit, the baseball metaphors, and the folksy wisdom of Warren. But with the release of the 2026 Letter to Shareholders, the tone has changed. For the first time, the signature at the bottom belongs to Greg Abel. Perhaps not yet worthy of being called the “Oracle”, I’ll call him the new “Operator of Omaha”. While Buffett was a storyteller, Abel is an operator. It is a big shift. In reading the first letter to shareholders recently by Abel, it sounds like the new operator of Berkshire has learned much from the retired Oracle and is focused the duties of stewardship and ensuring that the system Buffett built is “architecturally sound” for the next hundred years. Mr. Abel reinforced this with by introducing a stark warning against what he calls the “ABCs” of Corporate Decay:

Arrogance, Bureaucracy and Complacency. His focus is internal. He is signaling to the market that while the “Oracle” may have stepped back, the decentralization that made Berkshire great is being protected with a renewed, strict discipline. Here are some takeaways from the Berkshire Hathaway annual letter to shareholders penned by Greg Abel:

The Shift in Candor

We have always appreciated Buffett’s willingness to admit mistakes, but he often did so with a humorous “aw-shucks” anecdote. Abel’s candor is different—it is direct and corporate. His assessment of underperforming assets, specifically within the Kraft Heinz portfolio, was blunt. He noted that returns were “well short of adequate,” omitting the usual poetic cushioning. It is the language of a CEO who views every dollar of capital through the lens of a rigorous return-on-equity (ROE) mandate.

Arithmetic and the Cash “Moat”

Perhaps the most grounded moment of the letter was Abel’s acknowledgment of his own “simple arithmetic.” At 63, he noted he won’t be at the helm for another 60 years. By stripping away the symbolic past of the “immortal” leader, he forced shareholders to look at the balance sheet instead. With a cash pile near $380 billion, Abel has redefined “dry powder.” In this new era, that cash isn’t just a waiting room for an acquisition; it is a strategic moat designed to provide Berkshire with absolute optionality during the “extreme scenarios” that Abel seems to believe are inevitable in the coming decade (that sounds a lot like his old boss).

The Investment Takeaway

For shareholders, the takeaway is clear: The “Buffett Premium” may be fading, replaced by an “Institutional Discount” as the market adjusts to a leader who is less of a celebrity. However, if Abel succeeds, Berkshire will prove it is no longer a “one-man show” but a self-sustaining machine. The company is diversified, disciplined and Abel is determined. “BRKB” remains a core hold in Blackhawk Wealth Advisors’ Diversified Value portfolio.Abel isn’t promising us magic; he’s promising us math. In an increasingly volatile market, that might be exactly what the doctor ordered. I think he has the makings of a good operator.

|

|

|

Proper Perspective: In our hectic and often hard to comprehend world, it is very easy to lose perspective. You may agree it is sometimes difficult to see the big picture. The media often doesn’t help with this, but unfortunately instead encourages us to see things in a most negative light. Here is hopefully a pause to gain positive perspective.

|

|

|

Famous Quote For Today: “The quality of a play is the quality of its ideas.”

~~ George Bernard Shaw, 1950

Today in History – On this day in 1914, US Congress establishes Mother’s Day.

|

|

|

INDICATORS OF INTEREST:

- Market’s Current Signal: Confirmed Uptrend. Analysis of the stock market over 130 years of history shows we can view it in terms of three stages -market in uptrend, uptrend under pressure and market correction. Since the 1880’s, this perspective has led to investment out-performance relative to market indexes. This is due to trend analysis which determines risk reducing, return enhancing market entry and exit points.

The U.S. stock market’s current signal indicates the market is in Confirmed Uptrend. This trend change was triggered April 8, confirming a rally attempt on March 31. The bullish rally remains strongly intact. April was the best month for the stock market since 2020.

|

|

|

Here are key market levels as of Monday, May 4:

|

|

Recapping Last Week

U.S. equity indexes extended their April rally, rising modestly last week as the S&P500 and Nasdaq reached fresh record highs, led by Big Tech after stellar earnings boosted share prices. Ten of eleven S&P500 sectors finished higher on the week – materials were the sole loser. As expected, the Fed held rates steady, but votes on policy were more divided than in past meetings. Core PCE, the Fed’s preferred measure of inflation rose 0.3% MoM and 3.2% YoY. This reading was surprisingly tame given oil prices, but still complicated the future path of Fed policy. Speaking of oil, futures prices rose another 7% last week, clearing $110/barrel before settling near $100 as inventories in the U.S. dropped by 6.2 million barrels. The dollar index opened the week higher when U.S.–Iran talks stalled, but the buck faded through the week, helping gold, silver, and bitcoin hold steady. U.S. growth metrics remained strong, with Q1 GDP improving to 2.0% from Q4 2025’s 0.5% level. Durable goods and capital shipments showed continued momentum, and ISM Manufacturing PMI remained in expansion territory at 52.7. All 5 of the Mag 7 stocks that reported earnings last week beat expectations, but only AAPL, AMZN, and GOOGL saw a positive impact on their stock prices. Labor market data was mixed: at 189,000 jobless claims were at a 50-year low, yet the ADP employment reading pointed to a slowdown. Consumer confidence ticked higher and while housing prices are still up year over year, they were flat MoM.

Overseas, the Bank of Japan increased inflation forecasts but stopped short of indicating any rate hikes. Europe continues to lag. Although Germany posted modest growth, the broader Eurozone GDP disappointed, and unemployment ticked up to 6.2% giving the ECB more freedom to act than the U.S. Fed currently enjoys. Canadian and U.K. central banks held rates steady, and an increase in Australian inflation proved it’s a global issue that belies the argument that financial markets need interest rate cuts.

Current View

Last night’s headline: “Stock Market Indexes Nasdaq, S&P 500, Russell 2000 Hit Highs”. Indeed, yesterday was another bullish day. Strong earnings reports and weaker oil prices lifted the stock market yesterday. Increased hopes of a peace deal between the U.S. and Iran also added a boost to stocks – at least most, as energy stocks sold off. The Nasdaq composite sailed to new highs on Wednesday with a 2% gain to 25,838. That marked the fifth gain in six sessions as well as an all-time high or closing high in four of the past five sessions. The Dow Jones Industrial Average and other major stock indexes turned lower today, losing early mild gains as Wall Street digested initial unemployment claims data. Small caps fell the hardest. Cybersecurity firms were strong, though, as BAM positions CrowdStrike and Palo Alto Networks are up nicely. Earnings announcements continue to move stocks sharply up and down.

|

|

- Industry Group Strength: BULLISH. As of yesterday, 139 out the 197 groups I monitor are up year-to-date. 58 are down.

- New Highs vs. New Lows: BULLISH. In yesterday’s session, there were 279 new 52-week highs and 23 new 52-week lows.

- Dow Dividend Yield: BEARISH. The current yield for the Dow Jones Industrial Average is 1.78%. The 10-year Treasury now 4.40%.

- Volatility Index: BEARISH. Volatility has been volatile. The “VIX” is now 17. This is down from 19 two weeks ago. The index is also known as the “Fear Index.” It is considered a contrarian indicator and therefore viewed as bullish as it rises indicating investors are becoming more fearful. The VIX:

|

|

- Fear / Greed Index: BULLISH. Investors are driven by two emotions: fear and greed. Too much fear can create a condition of oversold/ undervalued stock prices. Too much greed can result in overbought/overvalued stock prices. The AAII Investor Sentiment Index is now neutral. BE FEARFUL WHEN OTHERS ARE GREEDY. At 68, the Fear & Greed Index is the same as 68 two weeks ago.

|

|

|

CLICK VIDEO FOR MORE ON THE “FEAR & GREED INDEX”

|

|

- Bull / Bear Barometer: BULLISH. This secondary market indicator should also be viewed with a contrarian perspective. As of yesterday, according to the latest survey of stock market newsletter writers by Investor’s Intelligence, the bullish tally is 47.3%, down from 48.1% two weeks ago. The bears are 23.6%, up from 21.1% two weeks ago. Consider this a contrarian indicator because the crowd is often wrong at market tops and bottoms. In other words, extreme bullishness has been seen near several market tops in the past, while extreme bearishness has been seen at market bottoms.

|

- Put / Call Ratio: NEUTRAL. The ratio of put-to-call options is .76, down from 0.82 two weeks ago. The put-call ratio tracks the mood of what options investors are doing, not just saying. They typically buy puts if they think a stock will decline and calls if they think it will rise. If they’re buying lots of puts, they see the market declining. And if they’re loading up on calls, they’re generally bullish. Historically, market bottoms occurred when the reading spikes to 1.2 or more. Market tops are often made when the reading is 0.6 or less. Note how reliable this is with respect to the February record low coinciding with the market high. Keep in mind this is also a contrarian indicator.

|

|

|

Global Economic Indicators & Analysis:

POSITIVE INDICATORS

|

|

GDP Up: Real gross domestic product (GDP) increased at an annual rate of 2.0% in the first quarter of 2026, according to the advance estimate released today by the U.S. Bureau of Economic Analysis. In the fourth quarter of 2025, real GDP increased 0.5%. The contributors to the increase in real GDP in the first quarter were investment, exports, consumer spending, and government spending. Imports, which are a subtraction in the calculation of GDP, also increased.

|

|

Consumer Confidence Up: Confidence Inched Higher Despite Spiking Prices Amid Middle East Turmoil. The Conference Board Consumer Confidence Index® edged up by 0.6 points to 92.8 in April, from 92.2 in March’s upwardly revised reading. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—retreated by 0.3 points to 123.8. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—rose by 1.2 points to 72.2. The survey period for this month’s preliminary results was April 1–22, a period that included the temporary two-week ceasefire in the Middle East conflict beginning April 8 and the subsequent rebound in US equities.

|

|

Factory Orders Up: New orders for manufactured goods in March, up four of the last five months, increased $9.1 billion or 1.5% to $630.4 billion, the U.S. Census Bureau reported today. This followed a 0.3% February increase. Shipments, up five of the last six months, increased $8.8 billion or 1.4 percent to $633.9 billion. This followed a 1.7% February increase. Unfilled orders, up twenty of the last twenty-one months, increased $1.6 billion or 0.1% to $1,540.9 billion. This followed a 0.1% February increase. The unfilled orders-to-shipments ratio was 6.88, down from 6.92 in February. Inventories, up six consecutive months, increased $5.8 billion or 0.6% to $956.3 billion. This followed a 0.1% February increase. The inventories-to-shipments ratio was 1.51, down from 1.52 in February.

|

|

ISM Services Up: The largest part of the economy took a hit in April from the fallout from the Iran war, a survey showed, but businesses still grew at a fairly robust pace even as they turned more cautious. A survey of service companies such as banks, retailers and restaurants dipped to 53.6% last month from 54.0% in the prior month, the Institute for Supply Management said Tuesday. Any number above 50% means business is growing. The index has topped that key threshold for 22 straight months. “Geopolitical concerns remain in play for the near term, though thus far have had little if any impact on operations,” a top executive at a healthcare provider told ISM. “ Forecast is good for the next quarter.”

|

|

ADP Employment Up: ADP said U.S. businesses created 109,000 new jobs in April — the biggest increase in 15 months — in a sign a partly frozen labor market might be thawing out after a bout of tepid hiring. Wall Street forecasters had predicted a 84,000 increase in private-sector jobs last month. “Small and large employers are hiring, but we’re seeing softness in the middle,” said Nela Richardson, chief economist at ADP, the U.S.’s largest processor of company payrolls. ADP is a lead act of sorts for the official U.S. employment report due Friday morning. Economists predict a 55,000 increase in new jobs in April based on information collected by the Bureau of Labor Statistics. The ADP and BLS reports can vary widely from month to month, as they did in March, but they move in the same direction over time. The BLS report is more comprehensive and, unlike ADP, it includes government workers.

|

|

New Home Sales Up: Sales of new single-family houses in March 2026 were at a seasonally-adjusted annual rate of 682,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.4% above the February 2026 rate of 635,000, and is 3.3 % above the March 2025 rate of 660,000. Sales of new single-family houses in February 2026 were at a seasonally-adjusted annual rate of 635,000. This is 8.9% above the January 2026 rate of 583,000.

|

|

US Trade Balance Up: March exports were $320.9 billion, $6.2 billion more than February exports. March imports were $381.2 billion, $8.7 billion more than February imports. The March increase in the goods and services deficit reflected an increase in the goods deficit of $4.1 billion to $88.7 billion and an increase in the services surplus of $1.6 billion to $28.4 billion. Year-to-date, the goods and services deficit decreased $211.2 billion, or 55%, from the same period in 2025. Exports increased $100.2 billion or 12%. Imports decreased $111.0 billion or 9.1%

|

|

|

Jobless Claims Up: Today’s report showed the number of people claiming unemployment benefits in the US rose by 10,000 from the from the count in previous week, which tied for the lowest since 1969, to 200,000 in the last week of April. It was below market expectations of 205,000 to remain firmly under the recent and historical average. Meanwhile, continuing claims, which are a proxy for outstanding unemployment in the US, fell by 10,000 to 1,766,000 on the week ending April 25th, the lowest in over two years and contrasting with expectations of an increase to 1,800,000.

|

|

Job Openings Down: The number of job openings in the U.S. and the speed at which businesses hire to fill them are still depressed — a depressing thought for anyone looking for work. U.S. job openings fell slightly to 6.87 million in March, hovering near a postpandemic low, the government said Tuesday. That’s at the lowest level so far in 2026. Businesses boosted hiring in March to a two-year high of 5.5 million, but the increase was likely tied to a severe winter freeze in February that kept people off the road. Hiring in February was the weakest in 12 years, excluding the pandemic. Poor weather probably pushed some of that hiring into March. If the two months are taken together, hiring was still at a depressed level. If hiring is on the upswing, the evidence should come in the April employment report, due Friday, and the job-openings report for April, due a month from now. The best news on the labor market, as has been the case lately, was the still-low number of layoffs. Companies aren’t hiring much, but they are not firing many people either. The rate of layoffs rose a tick to 1.2%, but it has ranged from 1.0% to 1.2% for the past two years. The lowest rate on record is 0.9%, which was last reached in June 2024.

|

|

U.S. Productivity Slows: U.S. worker productivity growth slowed further in the first quarter, but a reversal was likely as businesses invest heavily in artificial intelligence. Nonfarm productivity, which measures hourly output per worker, increased at 0.8% annualized rate last quarter, the Labor Department’s Bureau of Labor Statistics said on today. Data for the fourth quarter was revised down to show productivity growing at a 1.6% rate instead of the previously reported 1.8% pace. The pace has cooled since the 5.2% surge in the third quarter. Economists polled by Reuters had forecast productivity increasing at a 1.0% rate. Productivity grew at a 2.9% rate from a year ago. Economists believe the adoption of AI will boost productivity and rein in labor costs. Unit labor costs – the price of labor per single unit of output – increased at a 2.3% rate last quarter. Fourth-quarter productivity growth was revised higher to a 4.6% pace from the previously reported 4.4% rate. Economists had expected unit labor costs to increase at a 2.6% rate last quarter. They grew at a 1.2% rate from a year ago. Hourly compensation increased at a 3.1% rate last quarter and grew at a 4.2% pace from a year ago.

|

|

PCE Up: The Personal Consumption Expenditures (PCE) Price Index measures the prices paid for goods and services by U.S. consumers, serving as the Federal Reserve’s preferred inflation gauge. As of March 2026, the annual headline PCE rose 3.5%, up 0.7% for the month, while the core PCE (excluding food and energy) was 3.2%, up 0.3% for the month It is released monthly by the Bureau of Economic Analysis.

|

|

|

Call me if you have any questions. I am always happy to help!

John J. Gardner, CFP®, CPM®.

|

|

|

Blackhawk Wealth Advisors, Inc.

|

|

|