|

Recapping Last Week

U.S. equities rose and interest rates fell after Federal Reserve Chair Powell stated, “the time has come for policy to adjust”, the most direct signal yet that the FOMC intends to start cutting rates soon. The Russell 2000 index jumped 3.5%, while the S&P500 and Nasdaq Composite gained 1.4%. Energy was the only S&P500 sector to finish negative, pressured by lower crude oil prices. U.S. Treasury yields eased across the curve after Powell also remarked in his Jackson Hole keynote that confidence has grown for inflation moving towards the Fed’s 2% goal. However, he also issued a note of caution on U.S. labor markets, indicating that the Fed’s focus has shifted to ensure the economy stays near full employment. Several data points released last week suggested that the jobs market may not be as strong as previous reports had indicated. The U.S. Labor Department, as part of its annual benchmark revisions to the non-farm payroll numbers, reported that actual job growth was nearly 30% lower in the 12-month period through March 2024. This was the largest revision since 2009, although it still represented more than two million jobs created. Additionally, a New York Fed survey showed a drop in employment along with a surge in those looking for work. However, a combination of a gradual (rather than sharp) economic slowdown and looser monetary policy may indicate a longer economic cycle and a more supportive environment for risk assets. In other news, U.S. business activity fell slightly in August but remained firmly in expansion territory, according to the S&P Global flash PMI index. Average prices charged for goods and services rose at a slower rate as businesses reported customers pushing back against high prices. Retail giant Target saw its shares soar after reporting better-than-forecast earnings and revenue numbers, but the company struck a cautious tone on its outlook. New and existing home sales rose in July as buyers took advantage of falling mortgage rates.

Internationally, the yen gained ground after Bank of Japan Governor Ueda signaled a path to future rate hikes if prices continue to climb. Japan’s core CPI rose 2.7% YoY, an uptick from the prior month. Canada’s annual inflation rate cooled to 2.5%, keeping a September interest rate cut on track. The country’s top two railroads locked out more than 9,000 workers on Thursday, triggering a potential rail stoppage that could damage North American supply chains. However, the Canadian government stepped in to reduce tensions, and a back-to-work order may be forthcoming soon. Finally, business activity in Europe and the UK showed surprising strength this month, although the former continued to be somewhat hampered by Germany’s manufacturing downturn.

Current View

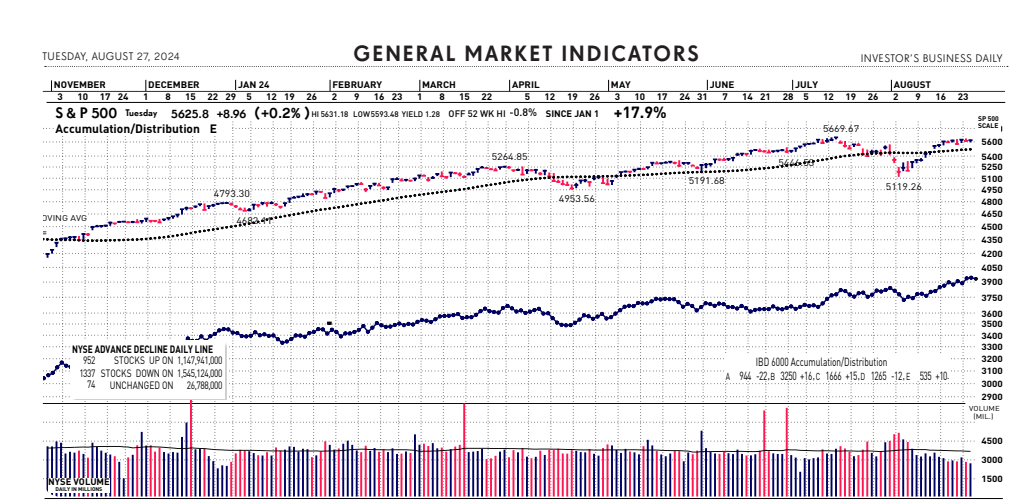

The stock market fell sharply yesterday as anxious and caution overtook a session that preceded one of the most consequential earnings reports with Nvidia’s quarterly results after the close. As if Nvidia’s report wouldn’t be enough, yesterday’s post-close earnings reports also included a leading Dow component, Salesforce, which is a major player in AI technology, and controversial CrowdStrike, releasing its first financial report since the global IT outage it caused. The tech sector fell about 1.5% on higher-than-average volume, resulting in a distribution day for the market. In the bond market, traders continue to price in lower interest rates. The 10-year Treasury yield is near its lowest levels of the year, at 3.84% late yesterday. The two-year Treasury yield, at 3.866%, is at the lowest since May 2023. In early morning trading today, the major indexes climbed even as influential artificial intelligence leader Nvidia fell following its earnings report. The market is solidly on track today to take-back yesterday’s losses. The participation in broadening and earnings and revenue growth, along with guidance, for the most part, have exceeded expectations. These factors have contributed to the current resilient market rally.

|