|

Bitcoin is a type of digital currency, known as a cryptocurrency. It was created in 2009 by an anonymous source using the pseudonym Satoshi Nakamoto. The Bitcoin cryptocurrency operates on a decentralized technology called blockchain, which is a public ledger of all transactions. This means it isn’t controlled by any government or bank, making it a peer-to-peer system for transferring value. People use bitcoin for buying goods and services, investing, and as a store of value. Its value has fluctuated significantly, as like anything else sold, is based on market demand. The supply side of the valuation equation is one unique feature of bitcoin. Its supply is limited. Bitcoin has a fixed supply of 21 million coins, which can help preserve its value over time. Over the past 16 years, bitcoin has grown from an unproven idea into a $2.4 trillion asset that is increasingly owned by some of the most respected investors in the world.

In recent years, bitcoin has emerged as a bona fide institutional asset. What was once a niche alternative asset owned mostly by retail investors is now broadly discussed and analyzed by the largest institutional financial firms around the world, and increasingly held by hedge funds, pensions, corporations, and sovereign wealth funds. The primary catalyst of broader ownership was the launch of spot bitcoin exchange-traded products in the U.S. in January 2024, which made accessing bitcoin safer, easy, and inexpensive for traditional investors. But the transformation has accelerated because of multiple factors, including the pro-crypto regulatory shift in the U.S. following last year’s presidential election. In January and March 2025, President Trump signed executive orders to make the U.S. the “crypto capital of the world”. The administration has voiced strong support for domestic Bitcoin mining. Trump has publicly stated that he wants “all the remaining Bitcoin to be MADE IN THE USA,” framing it as a national security issue. In July, President Trump signed the GENIUS Act into law. This is considered a broad victory for the crypto industry, providing regulatory certainty and creating the first federal framework for the asset class.

As bitcoin makes this transition to a more widely owned asset, there will be greater demand for long-term capital market assumptions. These robust, data-driven estimates of future returns, volatility, and correlations help investors model the role of bitcoin in portfolios. Here are some assumptions and investment perspectives that relate to bitcoin investing.

Capital Gain Assumptions

Return expectations are often expressed in terms of ROI (return on investment) over a period of time or as a CAGR (compounding annual growth rate), both stated in percentages. Due to the unique supply/demand dynamics of bitcoin, some analysts and experts often have varying outlooks, with some projecting future CAGR ranging from 20% to over 50% – depending on adoption rates, regulatory environments, and macroeconomic factors – over the next 10 years. Of course, demand and supply for the cryptocurrency will determine bitcoin’s future value.

Demand

While retail investors led its emergence, institutional investors are likely to maintain the highest demand for bitcoin going forward. The challenge, though, is approximately 95% of all the bitcoin that will ever exist is already owned — primarily by retail investors. So, institutional investors will have to buy bitcoin from existing investors. Even conservative demand assumptions from these investors – between 1% to 5% of their total assets – amounts to trillions of dollars. The World Bank believes that institutional investors control roughly $100 trillion in total assets. In the coming decade, that could mean investing $1 trillion to $5 trillion in bitcoin.

Supply

I noted above that there is a finite number of bitcoins. As of today, approximately 19.4 million Bitcoin have already been mined out of the total supply cap of 21 million. This means around 92-93% of all Bitcoin that will ever exist has been mined. Bitcoin’s supply is inelastic: No amount of demand for bitcoin or change in its price will cause more bitcoin to be produced, unlike gold, oil, or other major commodities.

Investment Perspective

A common question critics ask about bitcoin is: Why does it have any value? After all, bitcoin does not generate cash flows. In the view of bitcoin and cryptocurrency experts at Bitwise, the answer is… bitcoin as is a service. It has the ability to store wealth in a digital format without relying on a bank or a government. The more people who want this service, the more valuable bitcoin becomes. The fewer people who want this service, the less valuable bitcoin becomes. If no one wants this service, the value of bitcoin is zero. This is no different from any other service. The difference lies in how that value accrues. Using traditional software providers as an example, users who want that service pay an annual subscription fee to the company. With bitcoin, you can’t pay a subscription fee. After all, there is no “Bitcoin Company.” Instead, the only way to get the service is to buy bitcoin. If you buy bitcoin, you get the service—the ability to store wealth in a digital format without a bank.

Risk

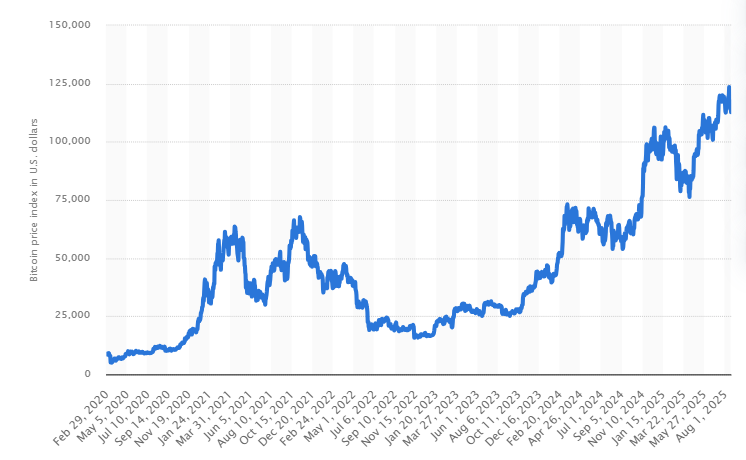

Historically, bitcoin has been a spectacular investment. The chart below shows its great gains since 2020. Like all investments, bitcoin certainly is not without risks. Bitcoin’s price can fluctuate wildly in a short period, leading to potential losses. Given its speculative nature, relying solely on price speculation without understanding the underlying technology or market trends increases risks associated with bitcoin. A unique risk to bitcoin is technological risk. Undiscovered flaws or future technological changes could render Bitcoin less useful or even obsolete.

|