|

Recapping Last Week

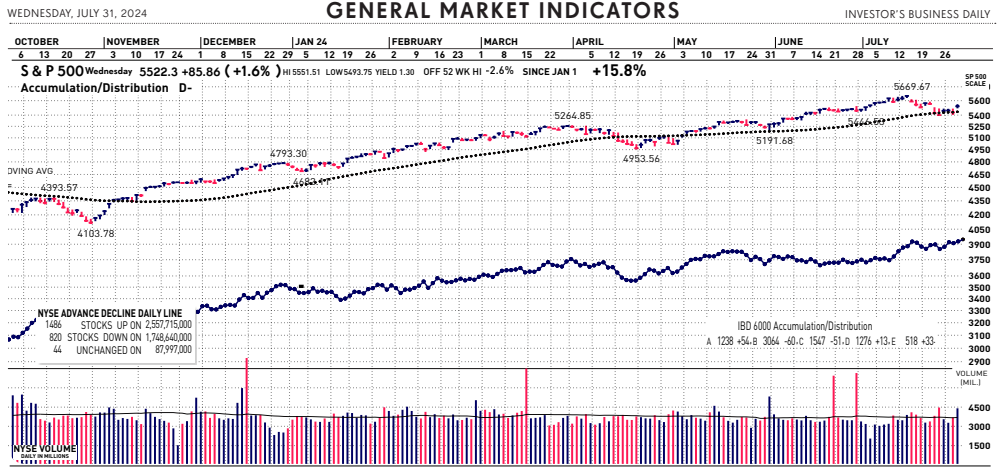

U.S. equity indices once again posted mixed performance in volatile trading as investors assessed the latest economic data and corporate earnings results. The Nasdaq Composite index fell more than 2%, while the S&P500 edged lower by nearly 1%. The Russell 2000, on the other hand, notchedits third straight week of gains, jumping 3.5%. S&P500 sector performance was spilt, with technology, communications, and consumer discretionary underperforming significantly. Disappointing earnings reports from Alphabet and Tesla sent the Nasdaq-100 index tumbling by more than 3.5% on Wednesday. Crude oil prices fell 2.3% as traders feared falling demand from China. U.S. Treasury yields retreated on Friday after June’s PCE index readings were in line with expectations, keeping on track a widely anticipated September interest rate cut. The headline inflation number was up 0.1% MoM and 2.5% YoY, while core PCE increased 0.2% MoM and 2.6% YoY. Personal income was below forecasts, with spending matching estimates. Data earlier in the week revealed that economic activity continued to surprise to the upside with inflation subsiding, which is music to the Federal Reserve’s ears. Second-quarter GDP grew at a 2.8% annualized rate, well above expectations and led by a 2.3% increase in consumer spending. The economic momentum extended into July, as the S&P Global flash composite PMI rose to 55 and the services sector reached a 28-month high of 56.0. Goods and services prices continued to increase MoM, but at a slower rate. Durable goods orders for June were up 0.5%, excluding the volatile transportation sector. However, U.S. housing remained mixed as sales fell and prices rose. New and existing home sales sliding in June. The median existing home price jumped 4.1% YoY to an all-time high of $426,900.

Internationally, China surprised markets twice last week with interest rate adjustments. First, the country cut benchmark lending rates for the first time in nearly a year as leadership faces potential deflation, surging debt, and trade tensions. Second, China’s central bank conducted an unscheduled lending operation at sharply lower rates to provide more monetary stimulus. Chinese stocks fell as investors feared the urgent action indicated the economy could be in worse shape than previously thought. Elsewhere, the Bank of Canada lowered interest rates for a second straight meeting, with officials signaling that downside economic risks may be building. Finally, flash PMI readings in Europe and the UK reflected diverging economic trends. Germany’s manufacturing activity plunged to new lows, while Britain’s saw the fastest growth in two years.

Current View

The major market indexes closed out July on a strong note yesterday. Driven mainly by rate cut expectations and Fed chair Powell’s perceived support for that, a broad, bullish rally nearly boosted the Nasdaq higher for the month. It was just fractionally lower for July. The dominant winner in July was the Russell 2000 index, underscoring the “Great Rotation”. Today, though, the indices reversed sharply lower and small caps got whacked on some disappointing news on the U.S. economy. The Russell 2000 led the sell-off in equities, falling over 3% by mid-morning trading.

|