|

Recapping Last Week

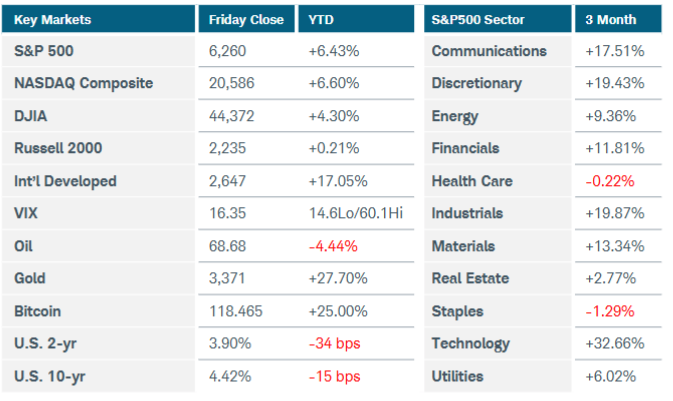

U.S. equity indices wobbled but still stayed near all-time highs despite additional trade war and tariff escalations. The S&P500, Nasdaq Composite, and Russell 2000 indices all finished marginally lower for the week. Six of eleven S&P500 sectors lost ground, including technology which failed to close higher even as Nvidia became the first company to exceed a $4 trillion market capitalization. In the commodity space, copper futures soared nearly 9% after President Trump proposed a 50% tariff on imports of the metal, which is a critical component of military hardware, electric vehicles, and many consumer goods. Gold futures rose more than 1% while silver prices spiked 5.5% to $39.15—their highest level since September 2011. Crude oil gained 2% after OPEC ministers and heads of western oil majors said that recent output boosts are not leading to higher inventories, which suggests an increase in global demand. Bitcoin jumped 7% to fresh record highs above $118,000. Auctions for 10- and 30-year Treasuries were met with solid demand but yields still pushed higher by week’s end. Aggressive tariff talk directed toward Japan, South Korea, Brazil, and Canada heightened inflationary concerns. The U.S. dollar also rose as currency traders speculated that tariffs may not damage the U.S. economy as much as initially feared and that interest rates could remain at or near current levels. Turning to economic data, Americans’ inflation outlook was little changed last month while households grew more optimistic on their finances, according to the New York Fed Survey of Consumer Expectations. Small business confidence slipped slightly in June as firms fretted over excess inventories. Minutes from the most recent FOMC meeting revealed that expectations for how tariffs might impact inflation differed. New rate projections showed that 10 of 19 officials expect at least two rate cuts by year-end, seven members project no cuts, and two members expect only one.

Overseas, Australia’s central bank chose to wait for more confirmation that inflation was easing before cutting rates, surprising market participants. Governor Bullock said the bank remained committed to loosening monetary policy provided that Q2 CPI is in-line with forecasts. China’s producer price index continued to tumble, falling 3.6% YoY in June. Consumer inflation edged slightly higher but domestic demand was still weak, adding pressure on policymakers to provide additional fiscal support. In Europe, the investor confidence index rose 4.4 points this month to reach its highest level since February 2022. Finally, Britain’s economy contracted for a second straight month in May, dashing hopes for Q2 GDP growth and adding to rate cut expectations.

Current View

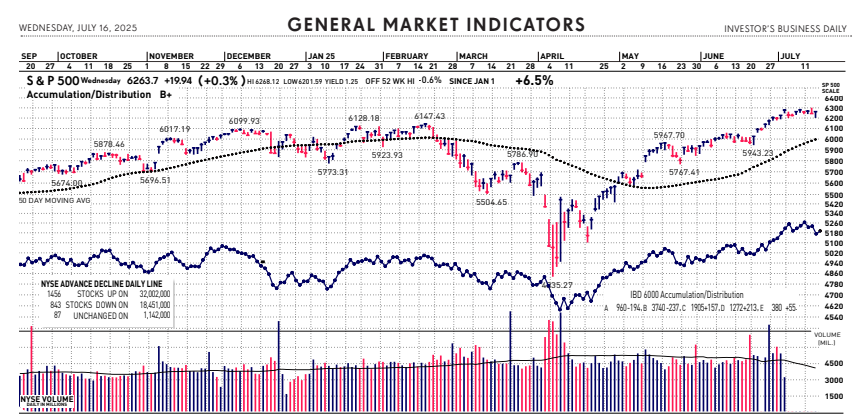

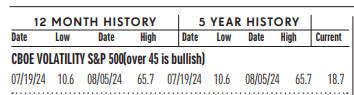

Small caps led another stock market rally Wednesday — and the major stock indexes closed near session highs — as Wall Street weighed another tame reading on inflation. Investors continue to shrug off the trade war drama, with the Volatility index falling to a five-month low of 15.70 last week. While the recent rally in stocks has been tested this week by a slew of economic data and corporate earnings announcements, so far it has passed the test. One day after a mostly in-line reading on consumer prices, yesterday’s analysis on wholesale prices didn’t raise any red flags. Prices in June were flat compared with May. That was softer than economist estimates for a gain of 0.2%. Overall, prices were up 2.3% year over year, below the 2.5% forecast. The drama du jour yesterday was an escalated version of the Trump Hates Powell show. A White House official told reporters that President Donald Trump was “likely” to fire Federal Reserve Chairman Jerome Powell “soon.” About 45 minutes later, Trump downplayed the statement from the Oval Office, saying it is “highly unlikely” he will fire Powell in the near future. Earnings announcement and tariff talks are likely to be the main market catalysts over the near term.

|