|

Internationally, Eurozone inflation came in higher at 2.6% YoY, but the European Central Bank is still expected to lower interest rates at the June 6 meeting. However, services inflation leapt to 4.1% from 3.7%, so additional cuts may be in doubt. In Germany, sentiment surveys stagnated, while retail sales slumped 1.2% in April. The IMF raised China’s economic growth forecast for this year and next, but disappointing PMI results for May implied that domestic demand is still lagging in that country. Lastly, core CPI excluding energy costs in Japan’s capital eased and factory activity fell, complicating the Bank of Japan’s plans to consider further interest rate hikes.

Current View

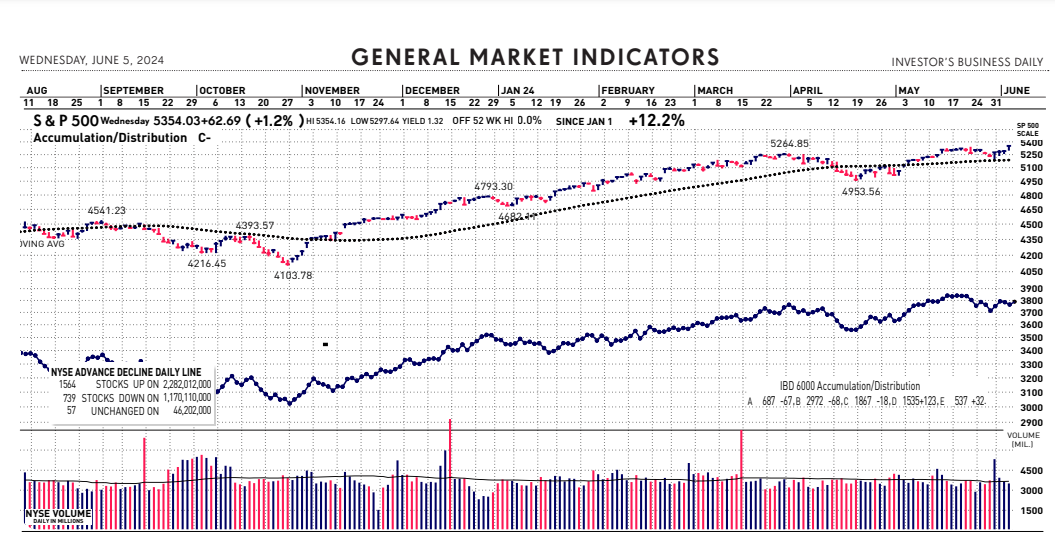

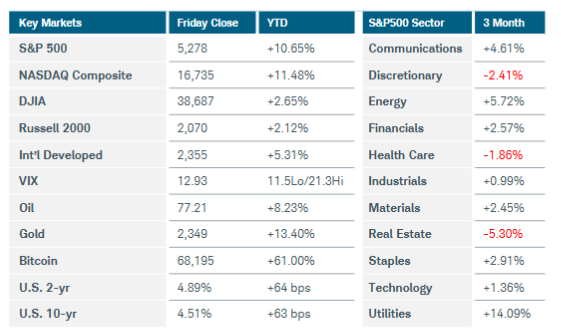

Growth stocks prevailed yesterday. The stock market displayed bullish action on a number of fronts: One, breakouts by highly rated growth stocks looked quite decent. Two, the Nasdaq and S&P 500, bastions of high-performance, high-growth companies, rose to all-time highs. A third and clear expression of growth stock leadership currently is yesterday’s market index action. The Nasdaq composite jumped 2% on a bullish increase in volume. At 17,187, it gushed to an all-time peak. The Nasdaq also lifted its year-to-date gain to 14.5%. The tech-rich index finished at its session high. That, offers a strong hint that institutional investors were loading up on growth stocks. Meanwhile, the S&P 500 rose 1.2% to 5354, also good for an all-time high. Volume on the New York Stock Exchange shrank modestly. In weaker action, the Dow Jones Industrial Average, full of blue chips that are not necessarily growing very fast, couldn’t seem to get out of its own way. The Russell indexes also reflected a lack of buying enthusiasm for so-called cheap stocks. So far this year the is up 3%. The Russell 2000 small cap index is just up 1.8%. Again, its the mega-cap techs stocks that are leading the bull market charge. The Semiconductor index(SOXX), dominated by its exposure to Nvidia, is up 26.4% through yesterday. The IShares Expanded Tech-Software IGV, is down 1.4%. So, not all tech stocks are up this year.

Bond markets reacted bullishly for growth stocks. How? For starters, the yield on the benchmark U.S. Treasury 10-year note dropped 4 basis points to 4.28%. Lower interest rates over a long time frame encourages stock investment, stock buybacks, acquisitions and continued cash dividends payments to shareholders. Also, some market participants still believe the Federal Reserve has both time and the motives to cut interest rates on the short end of the yield curve. According to CME FedWatch, fed funds rate futures activity pointed to a nearly 71% possibility that the Fed will trim the fed funds rate by at least a quarter point at the September 18 meeting. That’s up from a 47% chance a week ago.

|