|

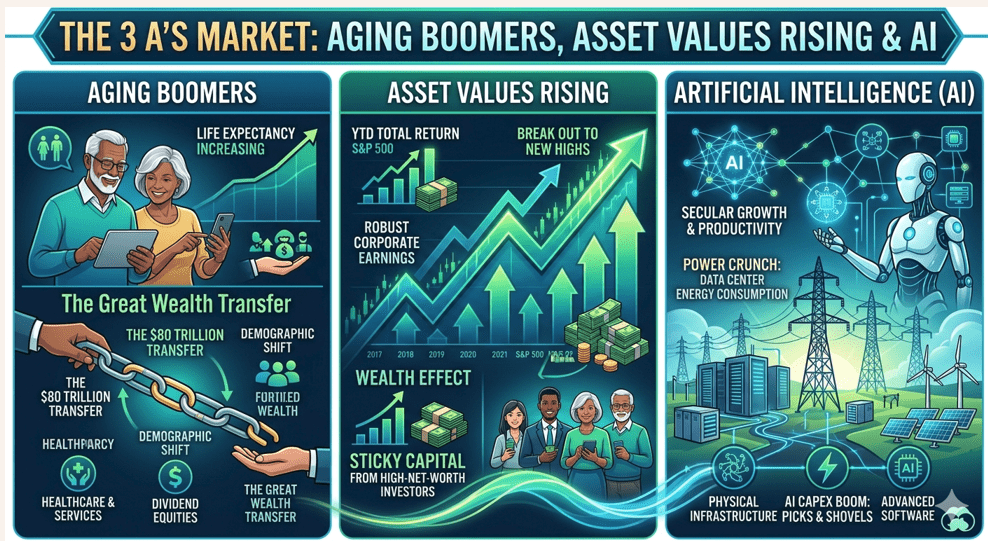

The U.S. stock market is now experiencing one of the greatest bull markets in history. Just a few quick stats: the SP 500 index rose last week for the 9th consecutive week, the longest win streak since December of 2023. This has only happened 10 times in history. If it closes this week higher, it would be the longest run up weeks since 1985. After the historic 10% rally in April, the S&P 500 added another 5% in May. This was the second-best April/May return ever, with only the 17.8% rally in 2020 better. What’s helping boost this bull? The current market cycle isn’t just about quarterly earnings beats and hope in Hormuz reopening soon. It is being propelled by three massive, interconnected structural trends: Aging Boomers, Asset Values Rising, and Artificial Intelligence. Together, they form the foundation of the “3 A’s Market”. Think of these three as the triple engines fueling the bull market…

Aging Boomers: The “Sticky Capital” & Spending Cushion

As of 2026, the very first Baby Boomers (born in 1946) are turning 80 years old. Boomers and older generations currently hold over $80 trillion in wealth. This generation comprises roughly 20% of the U.S. population (approximately 67 million people). Counter to old economic theories that seniors dump stocks the moment they retire, Boomers are actually acting as a major pillar of support for equities. With trillions remaining in retirement accounts, Boomers aren’t abandoning equities; they remain invested in high-quality, dividend-paying, and cash-flow-rich mega-cap stocks. This massive, institutionalized pool of “sticky capital” keeps a high floor under stock prices, dampening market pullbacks. And because this wealthiest demographic in history is sitting on over $80 trillion, they may be the most powerful of the three engines boosting the bull market. Their ongoing consumer spending power is impactful — particularly on healthcare, travel, and high-end services. This a solid backstop for U.S. GDP. This demand directly drives corporate revenues in many market sectors and industry groups.

Asset Values Rising: The Wealth Effect & Firing on All Cylinders

Despite persistent calls for a cyclical slowdown over the past couple of years, traditional equity assets have shown incredible resilience, driven by corporate profitability and solid economic foundations. the stock market is not the only asset class enjoying rising values; so is the real estate market. Rising markets cause the “Wealth Effect”. As portfolios, retirement accounts, and home equity values climb, affluent consumers feel wealthier, which directly translates into sustained economic activity and corporate earnings growth. This second catalyst of the current bull market is closely related to the first one – the Boomers. They have simply had the most time to accumulate and compound their net worth as they have mostly held stocks and real estate for decades and have benefited from exceptional asset value appreciation. This wealth effect is very real. The economic reality is it stimulates growth through increased consumer spending which is the most important leg of the “economic stool”. Another core reason this bull market has been so resilient is that corporate America has mostly maintained and expanded its profit margins. Companies aren’t just riding inflation; they are growing real earnings. When earnings grow, stock prices naturally follow. As I often say, “Earnings are the single most important determining factor of stock prices”. Then there’s the psychological effects rising asset values have on the stock market. For one, FOMO. The fear of missing out, an emotional market driver, lifts the stock market (at least over the short term). Rising valuations begets higher valuations as money that is out of an asset class flows in. This creates a self-reinforcing wave of buying pressure that drives the market to new heights.

Artificial Intelligence: The Ultimate Productivity & CapEx Multiplier

AI is the crown jewel of this bull market. It provides both the fundamental growth and the visionary narrative that historic bull markets feed on. Doesn’t that sound like something you would have heard in the late 1990’s? AI is phenomenal fuel for a bull market in stocks just like the internet powered the dot.com bull market of the 90’s. Every secular bull market needs a transformative narrative, and AI technology is this one’s. Investors are simply willing to pay a premium for companies that promise exponential productivity gains which can be seen in today’s rapidly expanding stock valuation multiples. Speaking of multiplying – money being spent (capital expenditures “CapEx) on AI is leaping by the hundreds of billions! I just read a research piece by Goldman Sachs saying they are now forecasting that the big spenders on AI will be a combined $5.3 TRILLION between 2025 and 2030. Their previous estimate was $4.5 trillion. This is staggering money. That cash is flowing directly into the bank accounts of infrastructure companies, energy providers, grid developers, and hardware manufacturers. This massive capital rotation is breathing prolonged life into industrial, materials, and energy sectors, widening the market’s breadth. Here’s perspective on the enormous AI cap-ex: Driven by the dot-com boom, telecommunication and broadband companies invested over $2.2 trillion in telecom and fiber-optic infrastructure to support the internet. This isn’t a fragile bull market built on cheap debt or central bank gimmicks like we’ve seen in past rising markets, it is being driven by the fundamental reality of the 3 A’s. Together, they create a highly resilient foundation for equities. However, as a mentor of mine used to say, “Trees don’t grow to sky.” There’s a limit all growth. The “Boom/Bust” cycle is also a reality. As we are living the boom now, we should be prepared for bust. FOMO can quickly turn into FOBI (the Fear of Being In).

|