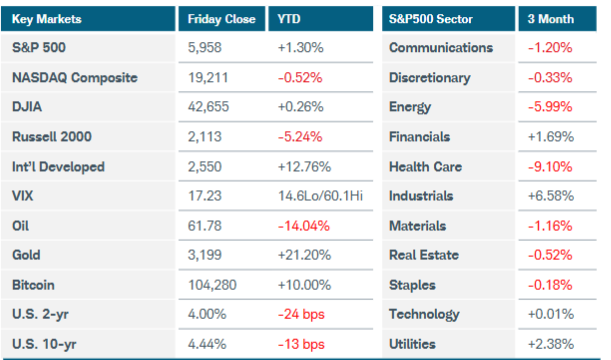

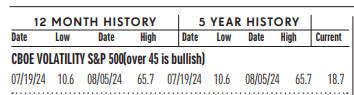

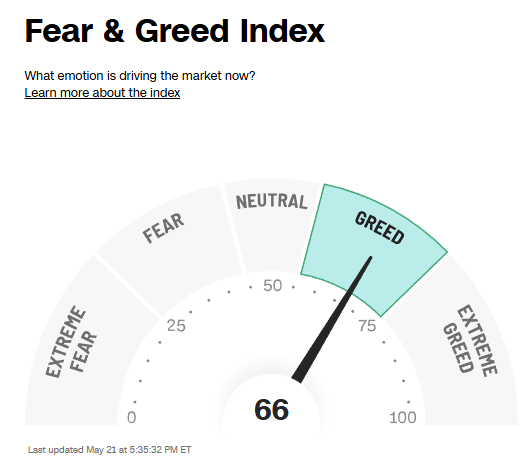

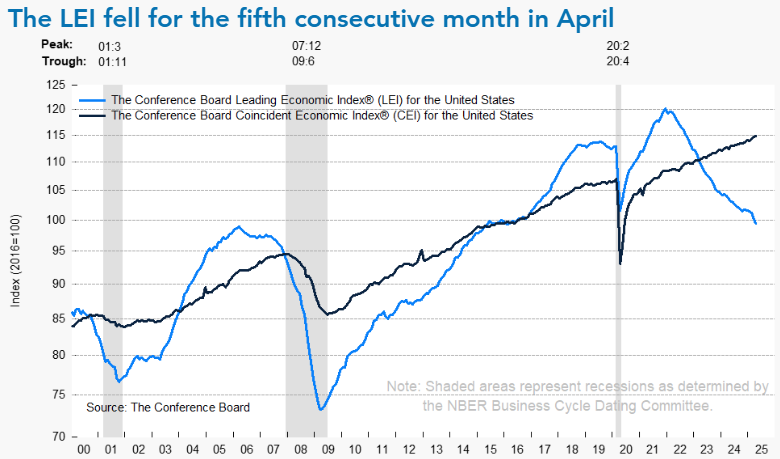

|

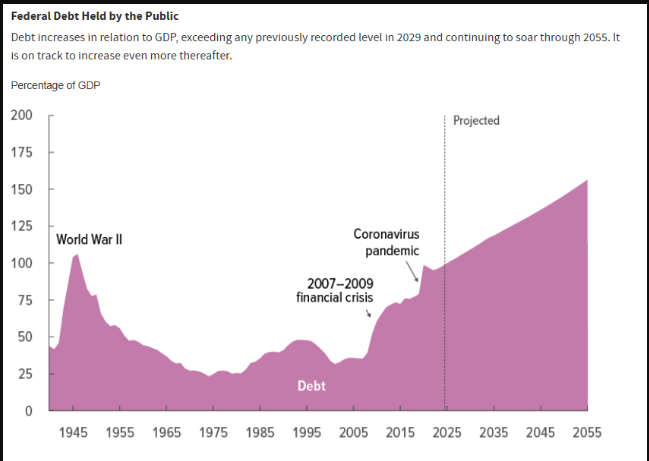

Yes, you should care about the U.S. debt downgrade. And so should the rest of American consumers and businesses, as well as investors worldwide. The potential result of this week’s U.S. debt downgrade by rating agency Moody’s is higher borrowing costs for all. While by no means does the U.S. bond rating downgrade suggest “junk”, the reduced rating knock down value of bond investments and others. Though the U.S. still holds a high credit rating, the downgrade signals a shift in perceptions of the U.S. as a safe and reliable borrower, which can affect interest rates on loans, bonds, and other investments. Thanks to Moody’s, the U.S. no longer holds the highest credit rating from any of the major agencies. The other two major bond rating agencies, Standard & Poor’s and Fitch, already dropped their rating on U.S debt instruments. S&P in 2011 and Fitch in 2023. Why have these graders of bonds all lowered their opinion and lost confidence in America’s bonds? Rising debt! The graph above indicates the rapid rate of U.S. debt increase since the late ’90’s and the projected trajectory of future increase. Here’s some reason’s the debt downgrade matters:

The country’s debt downgrade can lead to investors demanding higher interest rates on U.S. government debt, like Treasury bonds. These higher interest rates can then ripple through the economy, impacting borrowing costs for consumers and businesses, including mortgages, credit cards, and personal loans. The downgrade would likely cause US Treasury yields to rise as investors see more risk in lending money to the government. This includes bond buyers around the world.

Downgrades can create uncertainty in financial markets, making investors more cautious and potentially driving down the value of certain investments. The downgrade might also lead to a flight to safety, with investors seeking more stable assets like gold or foreign bonds.

Your investments, especially those in bonds or income-generating assets, could be affected by the downgrade. Rising interest rates can lead to a drop in the value of existing bonds. This is what I have long referred to as the “teeter-totter” effect. As interest rates rise, the price of bonds (and all interest-sensitive investments) go down. The downgrade could also make it harder for companies to borrow money, potentially impacting their stock prices.

- Potential for Economic Slowdown:

Higher borrowing costs can restrain economic growth by making it more expensive for businesses to invest and hire. The downgrade could also lead to a decline in consumer spending and confidence, further slowing down the economy. Plus, the much feared economic condition known as “stagflation” becomes a greater concern.

- Erosion of Confidence in the U.S. Dollar:

While the U.S. dollar is still the world’s reserve currency, a debt downgrade could weaken confidence in its stability and potentially lead to a decline in its value. This could make it more expensive for U.S. consumers to travel and purchase goods from overseas. Again, this could also impact the value of your investments as some prices move inversely to the dollar.

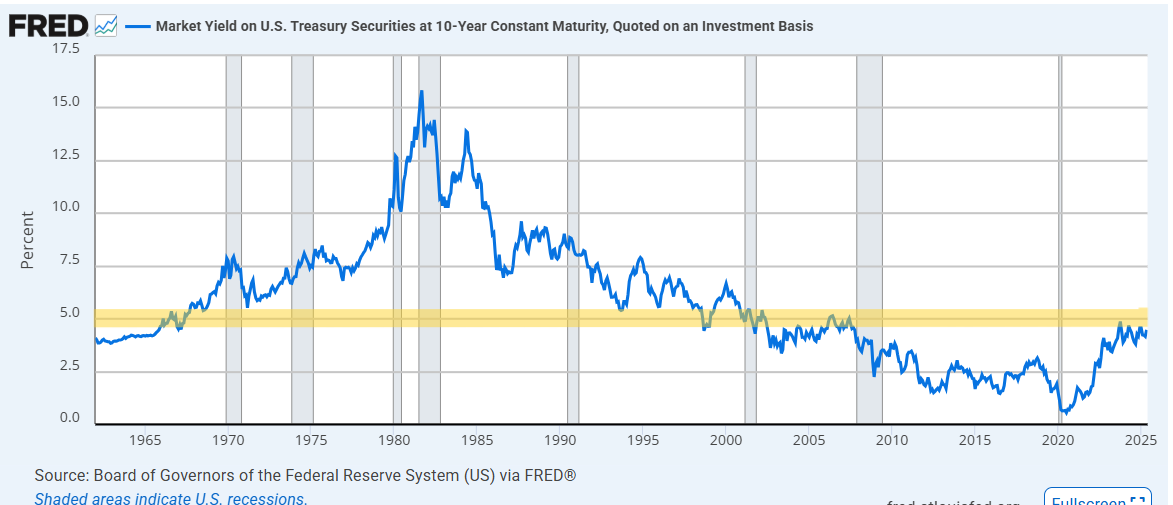

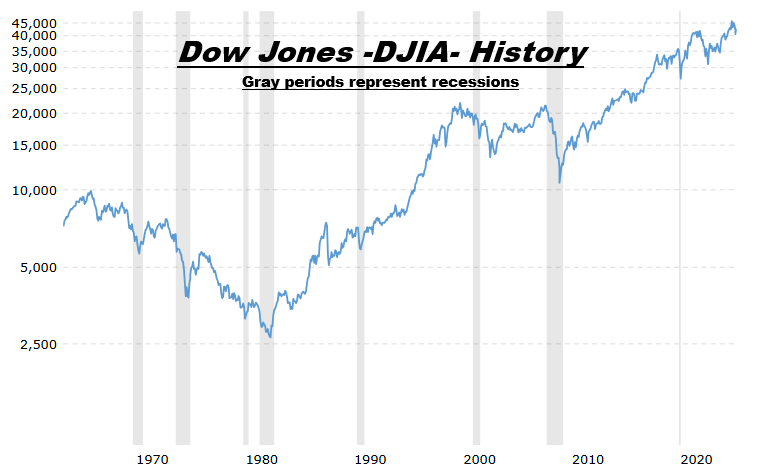

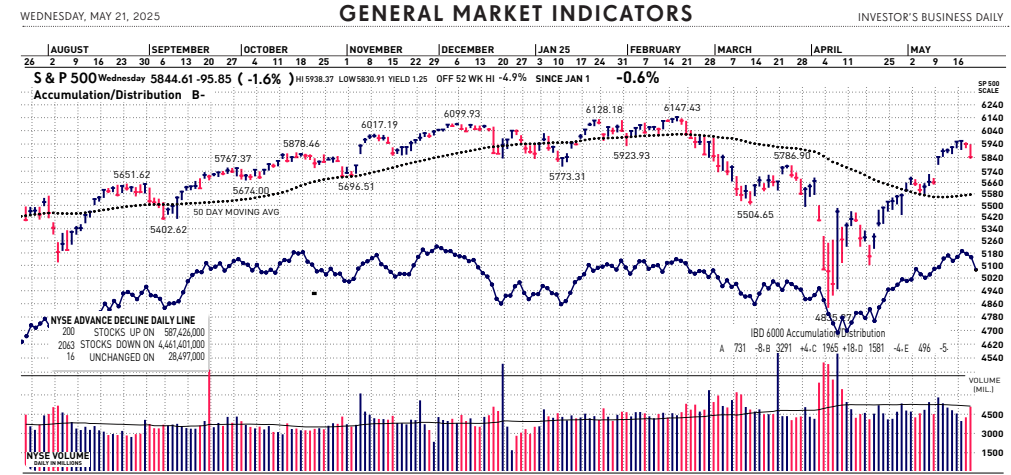

So, we know we should care and we can see why America’s credit lost its’ perfect, top-tier grade. The monumental deficit and mounting debt cost the U.S. the highest AAA status. That debt load, as predicted, is likely to rise. The Committee for a Responsible Federal Budget estimates that Trump’s “Big Beautiful Bill” would increase the deficit. “Overall, the bill would add more than $3.3 trillion to the debt over the next decade with interest – including $600 billion in 2027 alone – and add more than $5.2 trillion to the debt through 2034 if made permanent,” the committee said recently. As Republicans make progress on the President’s budget bill, bond markets are pushing back. That was evident in the financial markets yesterday. The plan includes tax and spending cuts, but would ultimately do little to curb the federal budget deficit. Some analysts, though, expect the budget plan likely won’t cause the deficit to increase. Further tax cuts will likely be offset by the administration’s new tariffs, there narrative goes…. “The upshot is that we expect the budget deficit to be broadly unchanged at close to 6% of GDP over the next few years, although that would still leave the debt burden on track to reach nearly 120% of GDP by 2034,” said one economist. I think a better choice to listen to for future market direction is the market itself, not the “experts” talking about it. The market’s message is clear: it does not trend up while interest rates are rising. The charts below show that. Notice the spike in the 10-year Treasury yield between the early ’70’s to the early ’80’s, and the relative market direction. That is an inverse relationship. Look at the yellow line the top chart yields at 5%. That is now the market’s focus. History shows stock market weakness when the 10-year is over 5% and trending higher.

|