|

Recapping Last Week

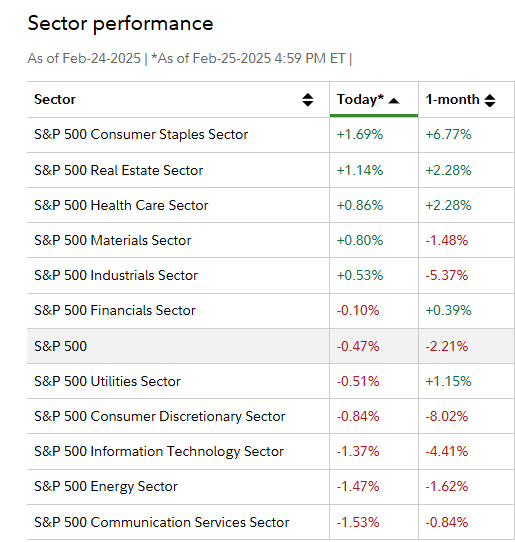

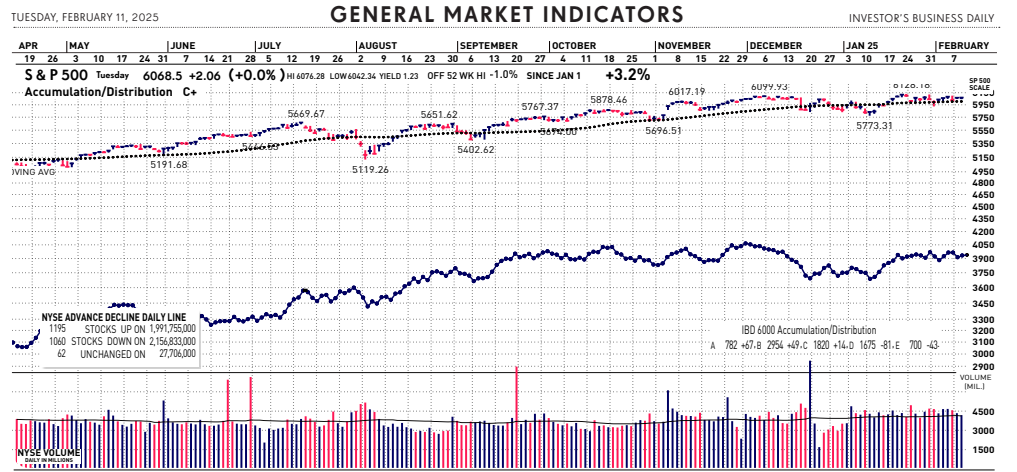

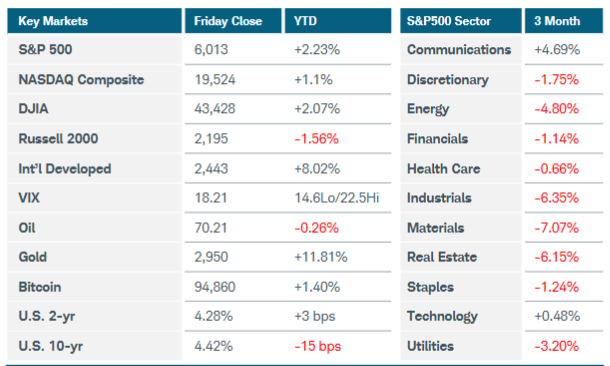

U.S. equity indices finished the week flat-to-lower as gains early faded into lingering inflation concerns to end the week. The S&P500 and Nasdaq Composite indexes fell 2%, while the small cap Russell 2000 lost 4%. Six out of eleven S&P500 sectors were negative on the week, while utilities and healthcare gained 1.5% and 1% respectively. Crude oil prices had another volatile week amid turmoil in Ukraine, yet finished mostly unchanged after reports of rising inventories caused a price pullback on Friday. Gold futures once again rose 2% to a new all-time high of $2973.40, edging ever closer to $3,000 per ounce. U.S. Treasury yields and the U.S. Dollar index both continued drifting lower, leaving the normal inverse correlation with equities at odds. Inflation and tariffs remain the main drivers of macro volatility. In Wednesday’s FOMC minutes, Federal Reserve officials seemed comfortable holding interest rates steady amid uncertain economic policies and slowing disinflationary trends. President Trump said he intends to impose tariffs “in the neighborhood of 25%” on automobiles and that he plans similar duties on semiconductors and pharmaceutical imports. Fed officials noted not only that these would lead to higher prices, but that the administration’s piecemeal approach is adding uncertainty about precisely which products would be affected. Headline U.S. PMI Index dropped to 50.4 from 52.7 in January, a 17-month low, and unemployment claims rose to 219,000, an increase of 5,000 from the week before. U.S. manufacturing data came in mixed as the Empire State Manufacturing Index popped to +5.7 in February from -12.6 in January, but the Philly Fed Index fell to 18.1 from 44.3 in January, the largest monthly drop in five years. The UofM Consumer Sentiment survey showed a 19% decline in buying conditions for durables, largely the result of fears of imminent tariff-induced price increases. Cost concerns are hitting the housing market as well, with the NAHB housing index dropping from 47 to 42. Existing home sales dropped 4.9% in January, though this level is still 2% higher than a year ago as prices increased for the 19th consecutive month. Housing starts slowed as builders pulled back amid concerns about mortgage rates and current inventory.

In international markets, Eurozone data is coming in more constructive, though inflation seems sticky in that region as well. UK CPI came in 3% higher in January vs 2.8% expectations, with some of that result coming from wages, as annual pay growth rose 5.9% from October to December. Retail sales rose by 1.7% as well. German PPI was 0.5% higher than a year ago, and their ZEW Economic Sentiment rose to 26, its strongest increase in two years. Australian and German PMIs were broadly expansionary yet showed a slight contraction in the UK. Australia’s unemployment rate ticked higher to 4.1% from 4%, and the RBA cut rates for the first time in four years while China left their rates alone. Inflation stayed front of mind in Canada and Japan, showing 1.9% and 4% increases respectively. This means headline inflation has been above Japan’s 2% target for 34 straight months. On the plus side, Japan’s economic expansion beat expectations in the fourth quarter when GDP grew 0.7% quarter-over-quarter vs 0.4% prior.

Current View

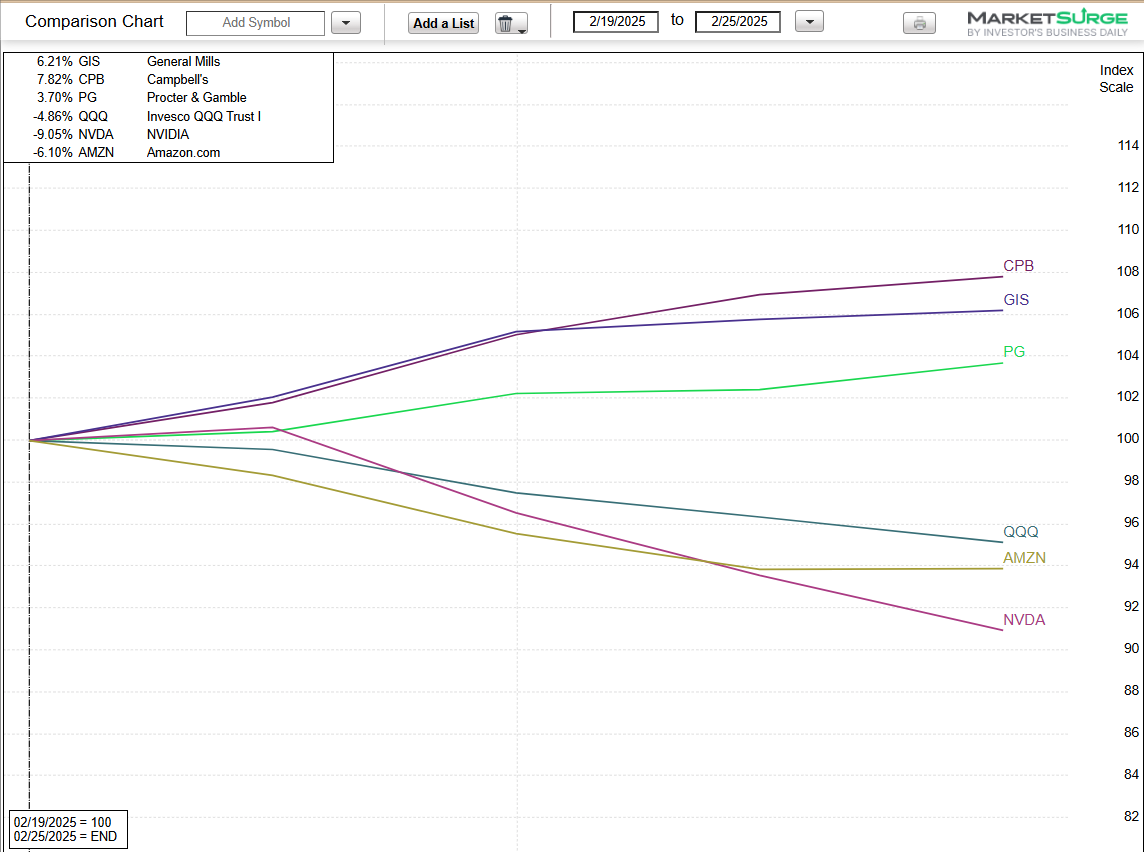

Early gains faded in the stock market Wednesday on more tariff talk, but Nasdaq 100 futures got a lift in after-hours trading when Nvidia (NVDA) delivered another strong earnings report. Strong opens and weak closes are typical in a weakening market, and that’s exactly what happened yesterday. After rising nearly 1.4% intraday, the Nasdaq composite closed with a gain of less than 0.3%. All eyes and ears on Wall Street were attentive to Nvidia’s earnings report after yesterday’s market close. After rising 3.7% during the regular session, Nvidia was up nearly 3% at one point in extended trading after reporting another quarter of strong bottom-line and top-line growth. Overnight that gain evaporated. This a another reminder of the stock markets extreme volatility lately.

The stock market started to weaken yesterday after 12:30 p.m. ET when President Donald Trump said that tariffs on European Union products would be 25% in general. He also said that tariffs on Canada and Mexico would take effect in early April. With increased volatility, investors may feel whipsawed. Tech stocks are especially displaying wild swings. Today, the Nasdaq reversed from an early-morning rise of nearly 0.9% to a loss of 1.4% at session lows. It would not be a surprise to see a positive close. That’s the type of volatile market we now have. The market’s trend signal is flashing Uptrend Under Pressure. The weaker signal would be Market in Correction.

|