|

Recapping Last Week

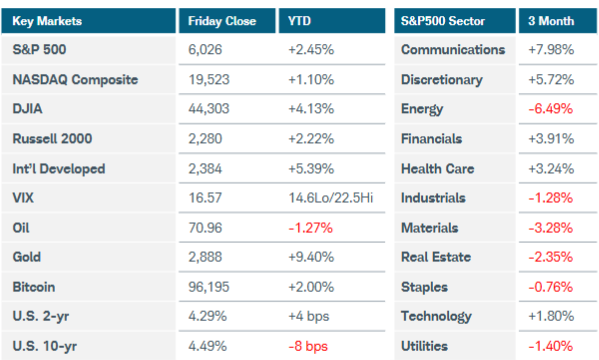

U.S. equities recovered most of Monday’s sharp selloff triggered by tariff announcements; however, the week ended on a down note after solid labor market data and an unexpected leap in U.S. inflation expectations. The S&P500, Nasdaq Composite, and Russell 2000 indices all fell marginally. Risk assets plunged to begin the week after the White House announced sweeping tariffs for Canada, Mexico, and China. Not long into the U.S. trading session, President Trump agreed to a 30-day pause for levies on Canadian and Mexican imports, which helped stabilize markets. However, China retaliated with tariffs on American imports and imposed exports controls on more key industrial elements. Eight of eleven S&P500 sectors gained ground, with technology rising nearly 1% despite subpar earnings reports from Alphabet and Amazon. Crude oil prices tumbled 4% after OPEC+ agreed to keep its policy intact of gradually increasing output, starting in April. A potential U.S.-China trade war also weighed on sentiment. Gold futures jumped 2% to a fresh record high and are nearing $3,000 per ounce. U.S. Treasury yields were lower for the week but spiked higher on Friday after the non-farm payrolls and consumer sentiment reports produced discouraging inflation news. Job creation was below expectations in January at 143k, but the prior two months were revised higher. Wage growth ticked up to 4.1% from 3.9% YoY, while the unemployment rate inched lower to 4%. Employers slashed jobs at the lowest rate in three years, according to the Challenger report. U.S. consumer sentiment for early February slumped to a seven-month low, with one-year inflation expectations shockingly surging to 4.3%—a full percentage point higher than the prior reading. The five-year inflation outlook rose to 3.3%, the highest reading since June 2008, as households feared the negative effects of tariffs. Other economic data signaled warning signs for price pressures as well. Non-farm productivity for Q4 2024 slipped to 1.2% from 2.3% as unit labor costs and hourly wages jumped. U.S. ISM manufacturing PMI moved into expansion territory at 50.9 last month for the first time in over two years, accompanied by a rise in the prices paid component. ISM services PMI slipped, but its prices index remained above 60 for a second straight month.

In international markets, the Bank of England cut interest rates by a quarter point to 4.5%. All nine members supported the reduction, but two surprisingly sought a larger reduction to 4.25%. The BoE cut its 2025 growth outlook in half but said it would proceed carefully with further policy moves, given an expected inflation spike and global economic uncertainty. Eurozone inflation accelerated to 2.5% YoY in January as energy costs rose. Germany’s factory orders jumped in December while industrial production declined, highlighting the mixed signals for the country’s beleaguered economy. Last of all, China’s Caixin PMI indices—which survey smaller, export-oriented companies—showed improvement in manufacturing while services missed forecasts. Investors will have to wait until the next reading to see if the recent Lunar New Year holiday spurred domestic demand.

Current View

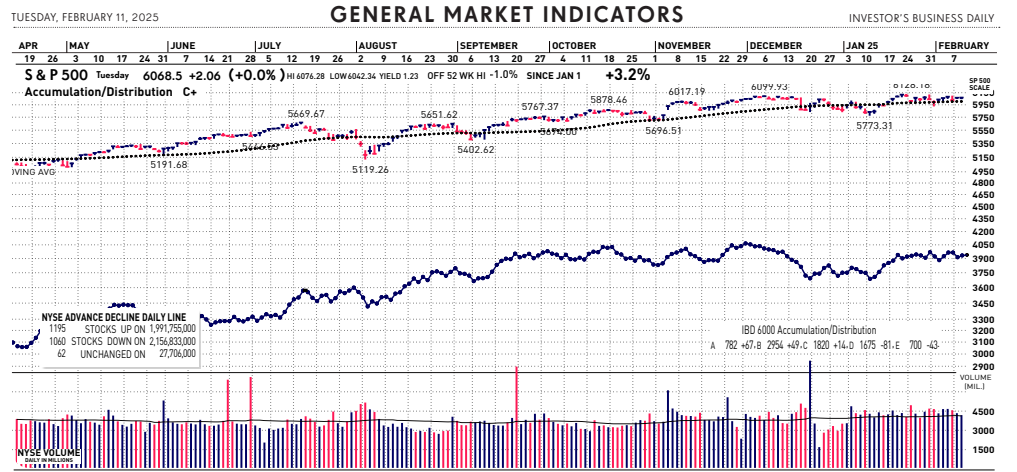

The current bull market continues to flex its strength with its resiliency. Yesterday is a another example in addition to similar bullish market action so far this year. Amid yesterday’s bullish reversal, the Nasdaq closed slightly above its 50-day moving average after spending most of the session below it. In another positive sign for growth leaders, the IBD 50 growth stock index outperformed with a 1.1% increase. The positive reversal is all the more impressive, considering that the yield on the benchmark U.S. 10-year government note spiked 10 basis points to 4.63%. At one point, the 10-year note yielded 4.66%. Meanwhile, bond traders are not seeing any real chance of a trim in the fed funds rate (currently at a target range of 4.25%-4.5%) until the September meeting.

|