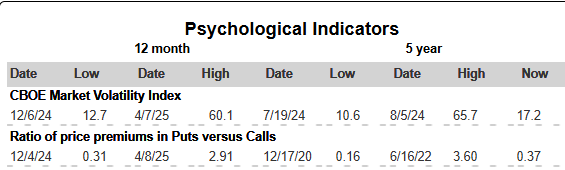

|

As we look forward to 2026, it’s worth reflecting back on the remarkable period we’ve just experienced. For the sixth time in seven years, the stock market has delivered double-digit returns, even though it hasn’t always felt smooth (this February, March and April are a great reminder of that). This has put many investors in a strong financial position, creating opportunities to make progress toward long-term goals.

What should we expect in the year ahead? While no one can predict the future with certainty, understanding the key themes shaping markets can help us maintain perspective and make informed decisions together.

2026 Outlook: Seven Key Themes for Long-Term Investors

1. Diversification is working again: For much of the past decade, U.S. stocks outperformed nearly everything else. That changed in 2025 as international stocks and bonds both contributed meaningfully to portfolio returns. Periods like the February through April stock market volatility remind us that a balanced approach can help smooth the journey toward your goals.

2. Stock valuations are elevated: Strong market returns have pushed stock prices higher relative to company earnings. The S&P 500 now trades at levels approaching those seen during the dot-com era, and we should be prepared for volatility as markets adjust to higher valuations. This simply means that investors need to be more thoughtful and selective when considering what a proper asset allocation looks like.

3. Artificial intelligence continues to drive growth: AI has captured enormous attention and investment. Companies are spending trillions building the infrastructure needed to support this technology. While AI will undoubtedly transform our economy, the key question is whether current stock prices already reflect this future growth. Since most portfolios have significant exposure to AI-related companies through major stock indices, maintaining appropriate balance remains essential.

4. Economic growth remains positive but uneven: The economy continues to grow at a healthy pace, though not everyone is experiencing this equally. Some sectors and income groups are thriving, while others face challenges. This is sometimes referred to as a “two-speed” or “K-shaped” economy. For investors, it’s important to separate what affects the overall market and how this might differ from our daily experiences.

5. Tariff concerns may continue: Despite significant attention in 2025, tariffs have not caused the economic disruption many feared. Inflation has remained relatively stable, and growth has continued. This doesn’t mean tariffs are unimportant, but it suggests that their effects may be more nuanced than headlines suggest. The key lesson is that we should not react to every policy announcement.

6. Political developments will create headlines: The upcoming midterm election, ongoing discussions about government debt, and the new One Big Beautiful Bill Act (OBBBA) tax legislation will all generate news throughout the year. While these topics matter for policy and planning, history shows that markets have performed well across different political environments. What we can control is ensuring your financial plan takes advantage of new tax rules. Now is a great time to check your plan!

7. The Federal Reserve will continue supporting the economy: With new leadership coming to the Fed in mid-2026, monetary policy will likely evolve. However, history shows that the economy has grown across different Fed chairs nominated by both political parties. Sticking to long-term financial goals, not over-reacting to monetary policy changes, is key.

Maintaining Perspective in 2026

Perhaps the most important lesson from recent years is that what investors fear most often doesn’t come to pass. This doesn’t mean we should ignore risks. Elevated valuations, slower global growth expectations, and various uncertainties all deserve continued attention. It is how we manage these risks but still move forward that really matters. I have always believed it is not what happens to us in life – but how we handle it, that matters.

The challenge for long-term investors isn’t predicting which specific events will matter most. Instead, it’s maintaining a balanced, diversified portfolio positioned to weather various outcomes while capturing long-term growth. After all, markets don’t move in straight lines.

In summary, markets have delivered strong performance, but the key to 2026 will continue to be maintaining a risk-aware portfolio aligned with your goals. As always, I’m here to help my clients navigate the year ahead and keep their financial plan on track.

What events might impact markets in 2026?

History shows that each year comes with new surprises that are often hard to predict. As we look ahead to 2026, several key factors could shape markets and the economy:

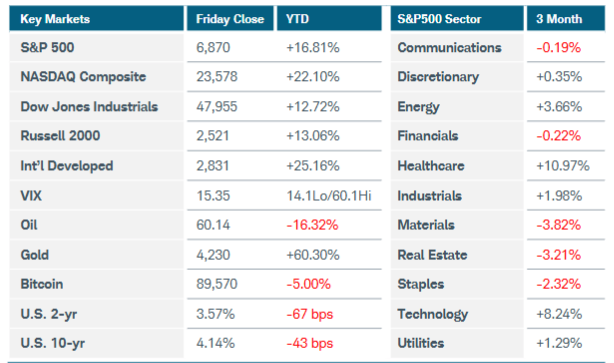

• Unlike much of the past decade when U.S. stocks dominated, many different asset classes are now contributing meaningfully to portfolio returns. International stocks have outpaced U.S. markets in 2025, with developed and emerging market stocks each gaining around 30%. Fixed income has also played its stabilizing role, with bonds also delivering positive outcomes for investors.

• The upcoming midterm election could have implications for tariffs, regulation, and government spending. Historically, midterm election years have delivered healthy market returns, with the S&P 500 averaging 8.6% since 1933. While political uncertainty may create short-term volatility, markets have historically looked past election cycles and focused on underlying economic fundamentals.

• Artificial intelligence remains a driving force shaping both the economy and markets. While this creates opportunities, it also means many portfolios have significant exposure to technology companies through major indices. The key is ensuring your portfolio remains appropriately balanced for your goals rather than becoming overly concentrated in any single theme.

The most important consideration isn’t predicting which of these factors will matter most, but ensuring your portfolio is positioned to weather uncertainty while capturing long-term growth. As I often say, the right question is not, “How is the market doing?” It is, “How is your plan doing?”.

This commentary is prepared for informational and educational purposes only and is not intended to provide financial, accounting, tax, or legal advice. It should not be used as the sole basis for any investment decision.

|