|

Recapping Last Week

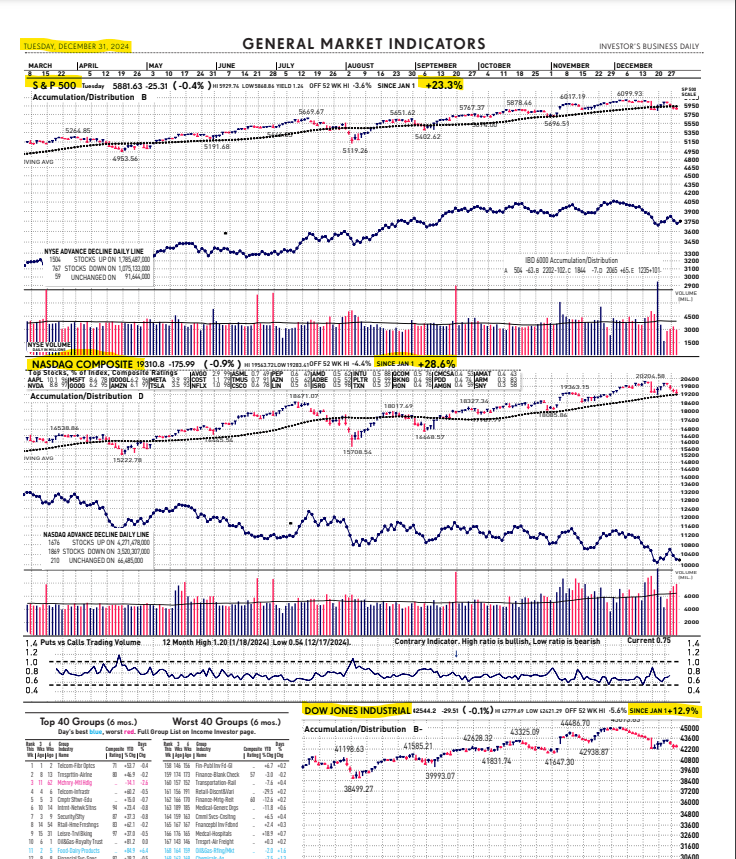

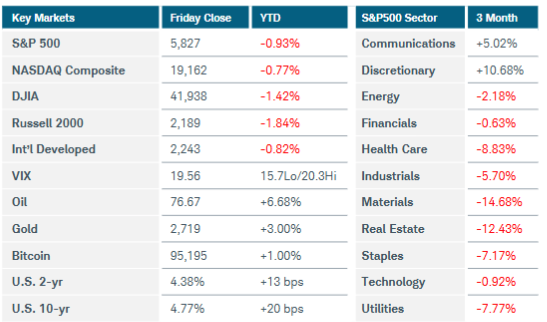

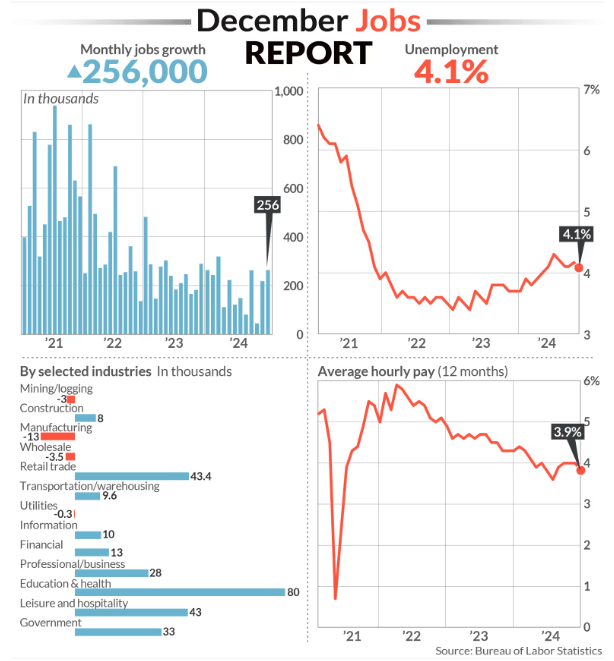

Stronger-than-expected economic data moved the goalposts for rate cuts this year, sending Treasury yields sharply higher and U.S. equity indices lower in a shortened trading week. The S&P500 index slid nearly 2%, while the Nasdaq Composite fell 2.3% and the Russell 2000 slumped 3.5%. Eight of eleven S&P500 sectors ended lower, with technology dropping 3% and real estate tumbling 4%. The energy sector was boosted by crude oil prices, which jumped more than 3.5% last Friday after the U.S. announced additional sanctions on the Russian oil industry, threatening supply constraints. U.S. Treasury yields spiked across the curve after December’s job growth came in much higher than forecasted. The 30-year bond yield surpassed 5% for the first time since October 2023 before retreating modestly. Non-farm payrolls expanded by 256,000 versus expectations for 155,000, while the unemployment rate edged down to 4.1% and the “under-employment” rate fell to 7.5% from 7.7%. Wage gains were muted—good news on the inflation front—but the overall stronger picture of the U.S. labor market caused traders to adjust their interest rate-cut assumptions. Fed funds futures aren’t pricing in more than a 50% chance of a cut until June, and sentiment has shifted to reflect only one potential cut this year, although it’s early and much can change. Other economic data supported the notion that the Fed’s easing policy may slow more than initially thought. Preliminary U.S. consumer sentiment for January slid to 73.2 as long-term inflation expectations jumped to 3.3% annualized, up from 3% just a month ago. ISM services PMI rose to 54.1 in December and the prices paid index leapt more than six points to 64.4, suggesting sharply higher costs for materials and services.

On the international front, China’s central bank outlined its 2025 priorities to promote a stable economy. Although the bank said it would implement moderately loose monetary policy to support growth, regulators sought to reassure investors last week as the country’s equity and currency markets extended losses. China’s stock exchanges asked some large mutual funds to restrict stock selling, while the central bank announced it will suspend buying government bonds as yields sank to all-time lows. Inflation in China remained subdued last month, raising the specter of deflation. Canadian Prime Minister Justin Trudeau said he would step down as leader of the ruling Liberal party but will stay in his post until a replacement is chosen, most likely in May at the earliest. European stocks and the euro initially rallied after some reports suggested that the potential U.S. tariff plan may not affect the region as extremely as feared. The gains were quickly reversed, however, in large part due to the U.S. dollar’s relentless advance. Eurozone inflation accelerated in December, but the move was anticipated and is unlikely to alter the central bank’s plans for more interest rate cuts.

Current View

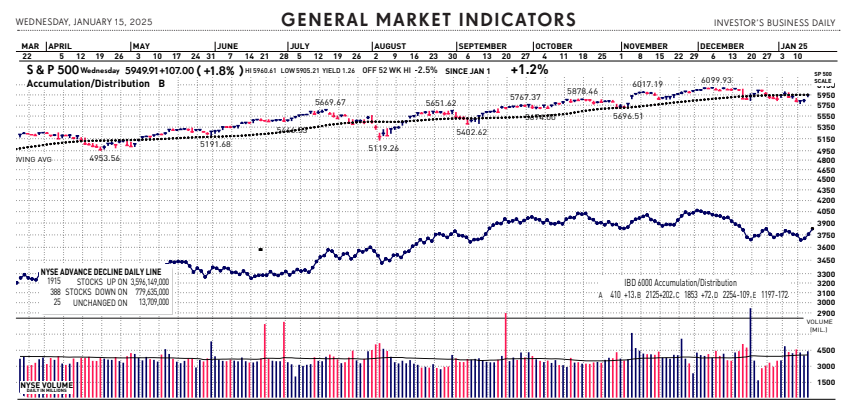

Yesterday’s major market indices were boosted by the two fundamental economic and stock market metrics; inflation and earnings. The back-to-back inflation reports Tuesday and yesterday confirmed cooling inflation. Earnings report from some of the largest banks exceeded expectations. The broad based market rally is in the spirit of the bull market that has run the last two years. Yesterday’s burst was led by the tech stock heavy Nasdaq index, which jumped 2.5% – the best day since November 6. While the current market trend signal reads “uptrend under pressure”, the market is showing resiliency and this week’s inflation data removed one brick from the market’s wall of worry.

|