|

Recapping Last Week

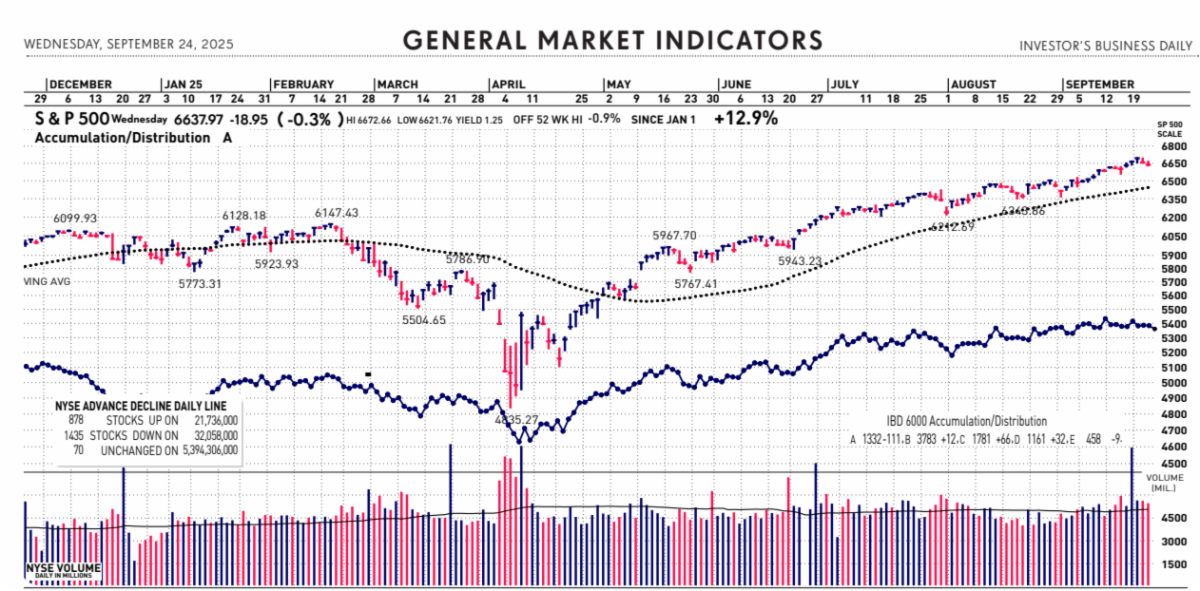

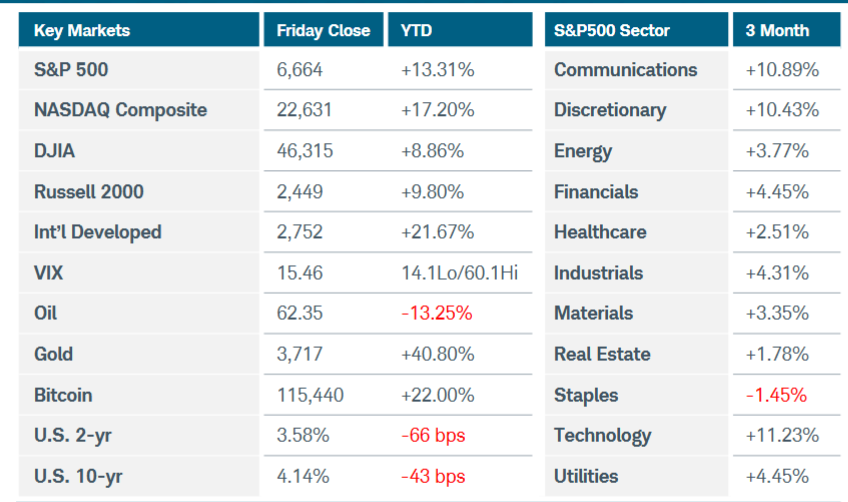

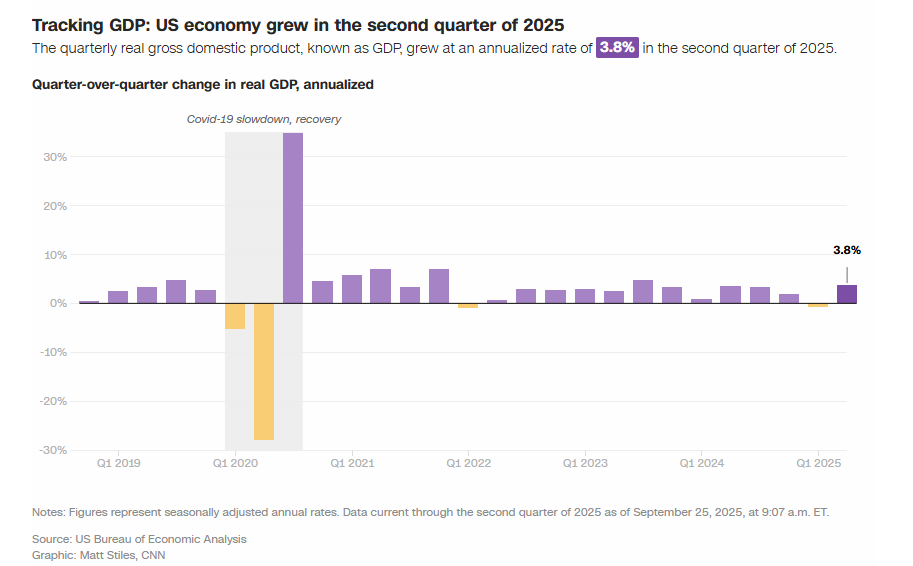

U.S. equity indices gained ground after the Federal Reserve restarted the interest rate easing cycle, lowering its benchmark rate by 25 basis points to a 4.00% to 4.25% range. The Russell 2000 index jumped more than 2%, reaching a new record high for the first time since last November. The Nasdaq Composite index also rose more than 2% while the S&P500 added just over 1%. Technology led mixed performance in S&P500 sectors, boosted by news of Nvidia’s massive investment in Intel. U.S. Treasury yields ended the week flat at the short end and higher at the long end despite the Fed signaling two additional rate cuts for this year. While Fed Chair Powell said that the softening labor market was now top of mind for the committee, the central bank’s statement acknowledged that inflation hasn’t just remained elevated but has moved up. Powell characterized the rate decision as a “risk-management cut” in reaction to weakening jobs data, but stubborn inflation underscores the Fed’s challenges in carrying out its dual mandate. In its Summary of Economic Projections, the FOMC raised its GDP growth and inflation forecasts while lowering the projected unemployment rate, seemingly in conflict with easing monetary policy. The updated “dot plots” suggested only one more rate cut in 2026 to a range of 3.25% to 3.50%, which is higher than market expectations of a sub-3% fed funds rate. Turning to economic data, U.S. retail sales rose 0.6% in August, rounding out a resilient summer of consumer spending. Jobless claims fell back to 231,000, likely confirming that the prior week’s large jump was an anomaly. Regional manufacturing surveys from the northeast revealed widely diverging sentiment. Activity in New York State declined more than expected on a large drop in new orders, while the Philly Fed survey spiked into positive territory as shipments surged. In housing news, new construction plunged last month while building permits fell to the lowest level in more than five years. Mortgage rates fell last week to 11-month lows, but persistent U.S. budgetary and inflation pressures still clouded the outlook for homebuyers seeking more affordable conditions.

Overseas, the Bank of England kept rates unchanged at 4% after last month’s CPI reading held steady at 3.8%–the highest among developed economies. UK labor market data has held up well enough to not raise recession concerns. The BOE also announced plans to slow the pace of reducing its stockpile of government bonds to minimize the impact on the volatile gilt markets. The Bank of Canada cut rates by 25 basis points to 2.5% but gave little indication of next steps even as economic data showed signs of increasing stress. Japan’s central bank revealed a more hawkish turn despite leaving rates unchanged at 0.5%. Two of the nine board members voted for a quarter-point hike while the Bank of Japan also decided to start selling its riskier ETF holdings sooner than expected. Core CPI readings have eased recently but Japan’s headline inflation has remained well above the 2% target for more than three years. Finally, China’s industrial production and retail sales figures for August came in lower than estimates, while unemployment inched up to a six-month high of 5.3%.

Current View

Since comments made by Federal Reserve Chair Jerome Powell in his Alan Greenspan moment during a fireside chat-style symposium in Warwick, R.I., saying the stock market is “fairly highly valued”, the major stock indices have mostly declined. Not that he is wrong, the market is overextended, but Greenspan was famously 4-years early with his call…. The Nasdaq, S&P 500 and Russell 2000 all finished above or very close to their short-term 10-day moving averages yesterday. While this is clearly a short-term observation, it is worth a look. The evidence is this moving average is experiencing the fastest rise in the slopes of these lines since early July. There has been a lot of bubble talk recently. Here’s perspective: When the Nasdaq-100 tech index peaked in March 2000, it was roughly 56% above its 200-day moving average. Today that number is closer to 13%. The current bull run in stocks hasn’t yet reached three years, given that stocks bottomed out in October 2022. Over the past 50 years, he said there have been five bull markets that lasted more than two years, and the average length was eight years.

|