|

Recapping Last Week

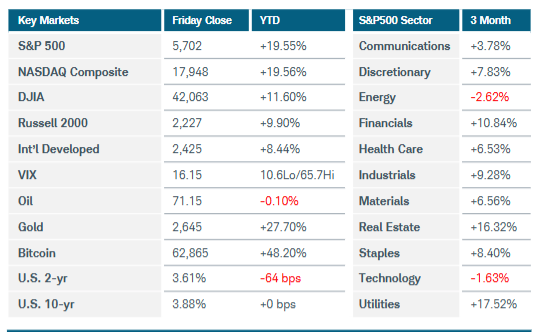

U.S. equities continued the prior week’s rally, reaching a new all-time high for both the S&P500 and the Dow Jones Industrial average. The Nasdaq-100 and Russell 2000 indices both posted solid performances as well, rising 1% and 2% respectively, but fell short of new all-time highs. The big story this week was Wednesday’s FOMC meeting. Everyone expected a rate cut was coming, but the devil was in the details. The FOMC opted for a 50bps cut versus 25 in an 11-1 vote and indicated another 50bps would be likely by the end of the year. Their Summary of Economic Projections report also revised down expectations for GDP and inflation. Stocks initially rallied but finished Wednesday’s session mostly unchanged. Thursday was more as expected with nearly all the week’s gains coming that day. Seven of eleven S&P 500 sectors were positive, led by energy, financials, and industrials with consumer staples and real estate falling behind, signaling a risk-on appetite to close out the week. Energy had a few positive catalysts, including geopolitical uncertainty in the Middle East stemming from exploding pagers, and the FOMC’s rate cut. The drop in the fed funds rate predictably put pressure on the U.S. dollar, which was supportive for other commodity prices, evidenced by oil and Bitcoin rallying between 2-5%. Yet, precious metals finished flat after posting large gains the week before. Other economic news in the U.S. was mostly positive starting with the Empire State Manufacturing index rising 16 points on Monday and the Philly Fed Index up 8.7 points Thursday, both newly into positive territory. Industrial production increased 0.8%, exceeding expectations, following a slide from the month prior due to Hurricane Beryl. The U.S. NAHB Housing Index beat expectations with participants noting the hope of lower interest rates on the horizon. Housing starts and permits rose 5% at the expense of existing home sales, which fell 2.5%. Lower rates are a bullish catalyst, but the median home price is still near all-time highs, deterring many potential buyers. Retail sales beat expectations along with an upward revision for July, and the good news continued Thursday with unemployment claims undercutting expectations.

On the international front, inflation and interest rates were also highly watched topics last week with CPI numbers and central bank meetings across the globe. Canada reached its 2% inflation target yet still plans to cut rates at each of its remaining 2024 meetings. In the U.K. consumer prices stayed flat, but services jumped 5.6%, leading the Bank of England to hold rates firm, and Japan followed suit holding rates steady after inflation met expectations, rising 2.8%. There were a few negative readings last week, starting with Germany’s ZEW Economic Sentiment falling from 19.2 to 3.6, reflecting the significant drop in German confidence and dragging Eurozone confidence down with it. China’s industrial output was the other negative mark, slowing to a 5-month low along with soft numbers in Chinese new home prices and retail sales.

This Week

This week kicks off with flash PMIs from all over the world, providing a glimpse into many areas like demand, employment, and price pressures. Australia, Germany, the U.K, the U.S, and Japan all release their purchasing managers index on Monday. All of those reports are expected to be very close to their previous readings, but the only ones above the 50-level, which indicates expansion, are out of the U.K. and services from the U.S. and Germany. Australia will give the rate statement that the rest of the world released last week the same day as their YoY CPI. A few different consumer confidence surveys will be released from Germany, and the U.S. is expecting numbers in line with recent reports. Fed Chairman Powell speaks on Thursday morning, but the most influential reports of the week will come Friday when U.S. core PCE and personal income and spending numbers are released. In July, PCE held unchanged and August’s expectations are no different, although they seem to be leveling off above the Fed’s long term target.

|